The moment has finally arrived. The Intelligent Fund Investor is published today!

Most of us invest in funds and the choices we make will have a profound impact on our financial futures. The problem is that fund investing is a decision-making nightmare. We are faced with a bewildering assortment of options and are constantly buffeted by market noise and narratives. Against this backdrop practising good investing behaviours is incredibly difficult.

Despite these challenges there are surprisingly few books available to help us with the unique set of problems fund investing poses. The aim of The Intelligent Fund Investor is to fill this gap. I hope it can help all types of investors avoid costly mistakes and make better decisions.

You can buy a copy here right now.

If you enjoy the book, I would be incredibly grateful if you could leave a review. If you don’t like it, please don’t tell anyone!

Month: November 2022

What Next for Defensive and Cautious Investors After a Torrid 2022?

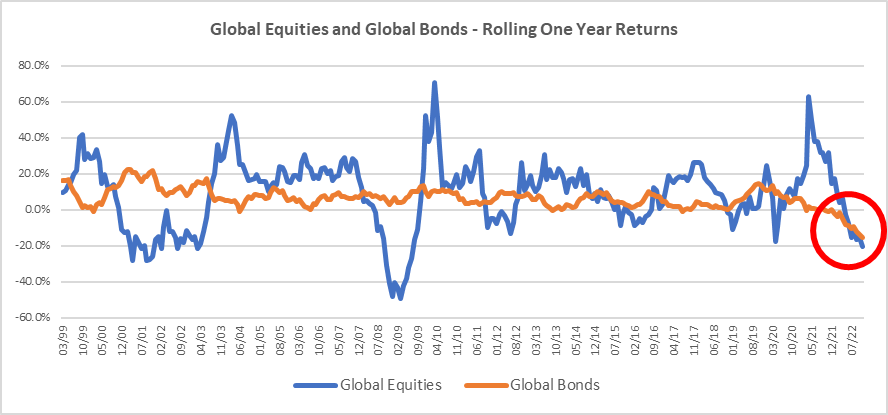

2022 has been an incredibly difficult year for investors. Not only have we seen steep declines in equity markets, but this has been coupled with sharply rising bond yields. The negative correlation between equities and high-quality bonds that has served investors well in times of stress has broken down, leaving many investors holding cautious and defensive funds nursing losses similar to those seen in far higher risk portfolios. Does this shift in asset class behaviour mean that cautious investors need to rethink their approach?

An Unusual Environment for Cautious Funds

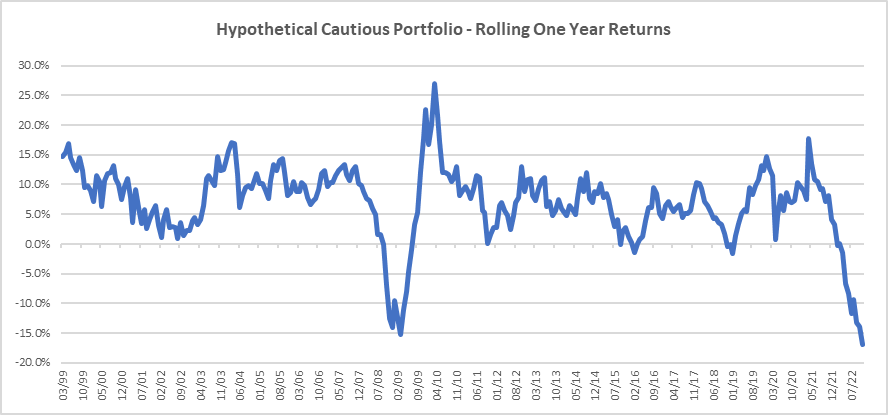

First, it is important to consider how rare the returns delivered in 2022 are for conservatively allocated investors. If we go back to 1999 – before the bursting of the tech bubble – and look at the one-year returns of a simple, hypothetical cautious portfolio (70% global bonds / 30% equities) * we can see how extreme the environment has been:

Losses are comparable with 2008 but have been generated in a very different manner. During the Global Financial Crisis equity returns were far worse, but some protection was provided by falling bond yields. In 2022, equity losses have not (yet) been comparable, but bond exposure has compounded investor problems, not mitigated them:

This is incredibly painful for cautious investors and has led to some results that are at the extreme end of reasonable expectations for this type of risk appetite. In such situations it is easy to make rash decisions, but it is crucial to reflect on what has happened and what the long-term implications may be.

A Valuation Windfall

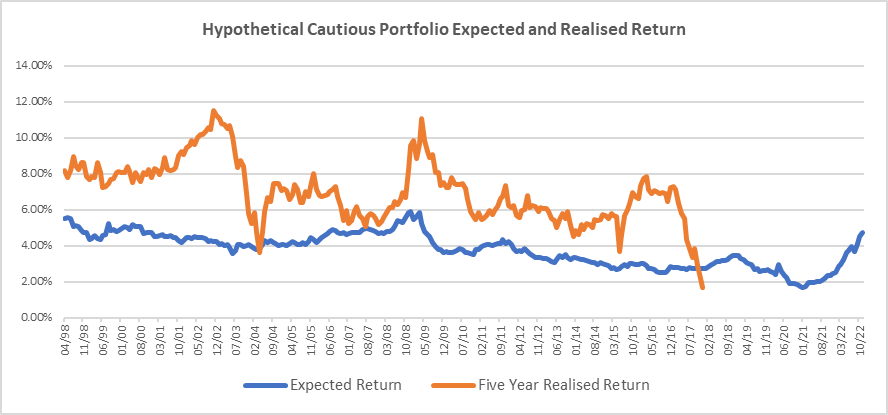

Over recent years a combination of falling bond yields and rising equity valuations has meant that cautious investors earnt returns that were higher than might have been reasonably anticipated from the cash flow prospects of their investments. We can visualise this by looking at a simple yield-based expected return for the hypothetical cautious portfolio (calculated by combining the earnings yield on equities with the yield to worst on bonds)** with the subsequent five year return delivered:

The blue line is what we might have realistically anticipated our return to be, given the yield of equities and bonds, while the orange line is the realised five year performance from that point. The realised return is five years out (on the chart the orange line ends in 2017/18, as it is the return five years from that point until today). The gap between the two shows that returns have been consistently above a reasonable projection of what such an asset allocation might deliver. This has been caused – at least in part – by what Antti Ilmanen of AQR refers to as a valuation ‘windfall’ – a one-off return that occurs when asset class valuations become significantly more expensive over a certain holding period. This type of performance tailwind does not persist forever and can move in the opposite direction if assets become considerably cheaper – as we have seen with bonds this year.

Periods of unusually high returns are often a prelude to weaker returns in the future. Although the human tendency is to extrapolate strong past performance, we should instead be moderating our expectations.

If Not Long Duration Bonds, Then What?

The cautious and defensive funds that have been most susceptible to losses in 2022 have been those using long duration bonds as a significant portion of their low-risk asset allocation – particularly those with a passive or quasi-passive approach. This strategy has been incredibly successful and effective for several years but did lead to many portfolios increasing their duration sensitivity as yields continued to fall (higher risk and lower returns, the so-called ‘return free risk’ trade).

Given the environment the results from many cautious funds this year should not be surprising – it is entirely consistent with their design – but does the recent experience mean that the approach adopted requires a rethink?

Not necessarily. No investment approach works in every situation, and we must be realistic about the drawbacks of any strategy in which we invest.

Much of the pain this year has been caused by being exposed to long duration bonds in an uncommon environment of sharply rising bond yields and declining equity markets. What options do cautious investors have if they wish to avoid this type of scenario?

Market timing: They could attempt to adjust exposures based on an assessment of the prevailing market environment. The problem is such tactical approaches are incredibly difficult to do well. The track record of investors making consistently successful interest rate and bond yield forecasts is poor.

Valuation-led approach: Rather than predict when things will occur as in a market timing strategy, they could adjust duration sensitivity based on the risk-reward characteristics of fixed income. For example, holding a short duration position when the yield available relative to the interest rate sensitivity is unattractive. The challenge here is that they must wait for valuations to normalise, and that can be a long wait.

Short duration: One option, particularly considering higher cash rates, is to run with a far shorter level of duration in their fixed income exposure, leaving them less sensitive to a more prolonged change in the relationship between movements in equities and bonds. Although this is a prudent approach, there are two potential drawbacks. First, if investors are comparing the performance of their cautious fund with a simple passive alternative there will be a large duration mismatch – are they willing to accept the underperformance that might stem from that? Second, in a recessionary bear market for equities we might again see significant declines in bond yields and their short duration approach may well offer us less protection in such a scenario.

Non-bond diversification: When bonds are failing to diversify our portfolios, particularly in difficult market conditions, there is always a great temptation to look for other sources of diversification. While this is a great option in theory there are dangers. There is often a temptation to invest in complex strategies that we do not truly understand, or asset classes that are not genuinely diversifying but simply look it because they are illiquid and have stale, mark to model pricing. Both scenarios lead to the assumption of a whole new host of risks.

As our tendency is to compare the (short-term) results of our cautious fund to a simple passive (equity / bond) comparator, adopting any of these approaches would have in all likelihood come with a prolonged and considerable performance cost in recent years. This does not mean all these methods are inferior, but investors need to be willing to bear the periods of underperformance that will inevitably occur.

There is a real danger that as investors we extol the virtues of a particular fund when it is delivering (often ignoring the inherent risks) and then abandon it when we are surprised by a period of poor performance. We are prone to adjust our fund holdings to deal with the risk that has just been realised, rather than those that may come to pass in the future. Consistently repeating this behaviour is likely to erode returns through time.

Deteriorating Performance and Improving Valuations

Given recent market performance there is a great deal of speculation about the negative correlation between equites and bonds that we have witnessed in recent decades being broken and becoming an artefact of an era defined by persistently falling bond yields. Whilst this is possible, it is extraordinarily difficult to predict with any level of conviction.

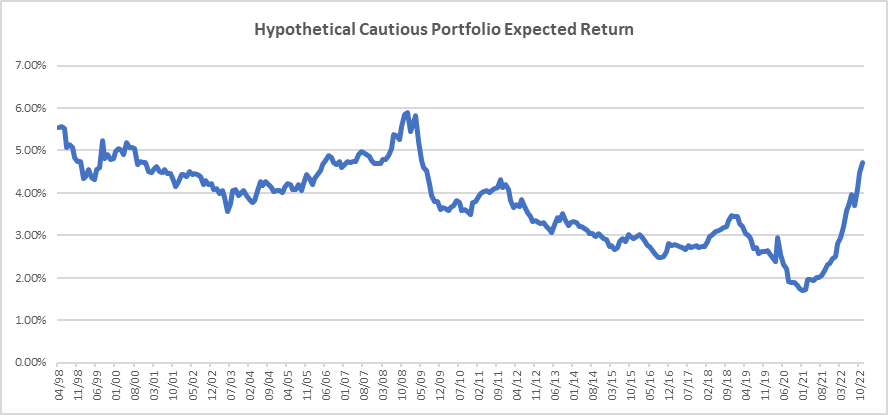

Rather than attempt to make such heroic forecasts, it is more prudent to look at areas where we can have greater confidence. The weakness in bonds and equities through 2022 means that our expected long-term returns for a typical cautious portfolio have improved significantly:

Unfortunately such valuation measures provide very little guide to the short-term outlook for cautious investors, but higher bond yields and lower equity prices do increase the probability of improved returns as we extend our time horizon.

Whichever approach to cautious investing we adopt, we need to understand both its benefits and limitations, and then decide whether we are behaviourally disposed to sticking with those for the long-term.

—

* The hypothetical cautious portfolio is comprised of a 70% allocation to a global aggregate bond index (USD hedged) and a 30% allocation to a global equity index. All returns in USD.

** This is a very simple model combining the earnings yields of equities and the yield to worst on bonds. It is meant to be instructive rather than a precise forecast.

—

I have a book coming out! The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can find out more here.

Investment Bubbles and Frauds Have a Lot in Common

Expensive investor mistakes come in two forms. We can either lose money slowly or quickly. Slow losses are small and compound over time – largely unnoticed – growing into a major cost; these can be through high fees or persistent performance chasing. Rapid losses are far more dramatic and are often a result of us having our investments unnecessarily concentrated in an asset class, fund or scheme that suffers a savage and irrecoverable decline. The most damaging sudden loss scenarios are typically investment bubbles and outright frauds. Although these two phenomena appear distinct, they exploit the same behavioural vulnerabilities.

An investment fraud is a situation where an individual (or group) makes a deliberate and nefarious attempt to mislead people about the characteristics of an investment for their own benefit. Contrastingly, an investment bubble occurs when there is a crowd delusion about the prospects for a particular security that sees its price detach from its underlying value by a dramatic margin; there may be disreputable individuals seeking to profit from a bubble, but no one person creates it.

Although these appear to be entirely separate episodes, they are deeply entwined. The life of an investment bubble or fraud is predicated on three critical aspects. The story, the performance and the social proof. These operate as a virtuous and vicious circle through the emergence and death of both bubbles and frauds:

Let’s take each element in turn:

Story: The narrative supporting an investment bubble or fraud is the critical underpinning. Stories not only provide a simple and compelling tale about why an investment opportunity is so attractive, they are also an incredibly effective means of disguising complexities and unpleasant realities. Successful stories make us blind to the risks and shortcomings. Tell us a gripping and believable story – one that ends with us making a lot of money – and that is often all we need to hear.

The influence of stories is intensified by the involvement of individuals with charisma. In frauds, they are often the person at the forefront telling the enthralling yarn, while in an investment bubble they are the main protagonists – the people that have already made a fortune and who we want to follow. Powerful storytellers and compelling characters make us even more susceptible to a story.

Performance: Strong past returns are also a vital feature of the most dangerous bubbles and frauds. This works in three ways:

1) It provides validation – we are so biased towards past outcomes that stellar recent performance is taken as a sign that something is being done right – otherwise why would it be working so well?

2) It allows us to extrapolate – we seem ingrained to believe that high returns from the past will continue unabated into the future.

3) It fosters greed – we are attracted to the high, often stratospheric, profits that have been delivered in the past and don’t want to miss out. The performance is far better than we are achieving in our own boring investments.

Social Proof: The behaviour of other people is also essential in the emergence and persistence of bubbles and frauds. It provokes both confidence and envy. Confidence stems from the idea that there is wisdom in the choices made by other people – this can be particularly true if institutions are involved – it must be okay because those smart people would have done the work. Envy arrives because we see other people making more money than us and cannot help but find it painful.

These three elements feed on each other. A captivating story both boosts performance and corroborates it (the story must be true, haven’t you seen the returns?); while strong performance increases the power of social proof (my friends are making even more money), and new investors becoming involved supports performance. This virtuous circle can be incredibly powerful and self-sustaining. The longer it persists, the more people are drawn in.

The failure of frauds and bubbles occurs when this circle reverts from virtuous to vicious and this can happen suddenly. The catalyst for this shift is impossible to predict. It can be a piece of news or information that punctures the story, or simply a period of poor performance that leads to doubt, scrutiny and, eventually, distress.

Bubbles and frauds not only prey on similar human behaviours, at times they can become one and the same thing. The most perilous situation is when a fraud morphs into a bubble. Here the euphoria that arises around an investment doesn’t lead to the price being detached from reality, but the price being attached to a fantasy.

For investors this is the worst of all worlds.

—

I have a book coming out! The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can find out more here.

The Power of Not Having a View

If you work in the investment industry then you must have a view. Always. About everything. When will inflation peak? Will the Fed pivot? How will Japanese equities fare over the next six months? Is Amazon expensive? Does this fund manager have skill? If we don’t have an opinion then we either lack knowledge or conviction, perhaps both. As professional investors this is what we are being paid for, isn’t it?

No, it isn’t. Quite the contrary. The ability to not have a view on most subjects is a major advantage, just one that is incredibly difficult to exploit.

There is a stigma attached to saying “I don’t know”, not just in the investment industry but in many walks of life. Nobody wants to sit on the fence or stand in the middle of the road, but for investors this is absolutely the correct place to be most of the time. We are operating in a highly complex, uncertain environment where most predictions are either difficult or impossible. Being well-calibrated means spending a lot of time not having an opinion.

The majority of investors have all sorts of views. Does this mean we are poorly calibrated? In many cases, yes. There are two reasons why investors are so keen to predict everything. The first is simple overconfidence – we think we are better than we are. The second is because it is expected of us – our clients want us to have a view, so we must form one.

Why is there an expectation for investors to have views on everything? Because it gives a sense of control. Financial markets are messy, chaotic, and anxiety-inducing; when an investor makes predictions and trades on them it feels like there is a steady hand on the tiller, rather than our portfolios being a hostage to fortune.

This is the enduring appeal of tactical asset allocation despite the compelling evidence that people cannot time markets successfully and consistently. Things are happening so investors need to be seen to be doing something about it.

But having wide-ranging and ever-changing views on markets is not harmless, it is damaging. Not only are investors constantly forecasting things when we cannot reasonably expect to have any skill in the task; it also means that we will be trading far more than is necessary – destroying value through transaction costs and the losses that stem from predicting the unpredictable.

The erroneous views that investors hold come in two forms. We can be operating far outside of our circle of competence – it is not feasible to have credible expertise in UK mid cap companies, the Chinese real estate sector, and the implications of the latest US non-farm payrolls report. Most common, however, is simply to have views on subjects that are not reasonably inside anybody’s circle of competence – typically these are short-term market perspectives: how is the Russell 2000 going to fare relative to the S&P 500 over the next six months? Who knows?

The vacillations of deep and intricate financial markets are endlessly fascinating but being intrigued by them does not mean we need to take a position or trade.

When Should Investors Take a View?

So if investors should avoid taking views most of the time, when should they do it?

The critical questions to ask are whether it is reasonable to have a view at all (is it something we or anyone can predict) and are the odds on our side in getting it right?

Let’s take an example.

I am asked to predict whether global equities will generate positive returns over the next six months. I have no idea. Over short run horizons markets are noisy and unpredictable, and I would simply be guessing with little confidence in my outlook.

But what if I am asked to predict whether global equities will generate positive returns over the next ten years. Here I have a view. Over the longer term the performance of equities will likely be driven by the cash flows they generate. History also tells me the odds are in my favour in having a confident (though not certain) perspective.

We should only express forthright views and take positions where we have a long-time horizon and a robust evidence base that suggests the likelihood of our view coming to pass is strong. This will often only occur when markets are priced at extremes, everything else we can think of as noise.

Wilful Ignorance

Not having an investment view on every imponderable in financial markets can seem like ignorance, but it actually shows an acute awareness of the environment in which we operate. It is far more ignorant to believe that we can accurately predict all manner of complex and unfathomable things.

Rather than have an ever-evolving set of views and positions, we would be far better off allowing others to pontificate and trade, and instead wait until there are opportunities where the probability of good outcomes are firmly on our side.

Investors would be far happier (and better off) not having a view on most things most of the time.

—

I have a book coming out! The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can find out more here.