When equity markets are rising it is really easy to stick with the key principles required to be a successful long-term investor; unfortunately, it gets far harder when they start to fall and uncertainty climbs. At the exact time when discipline is required, it can so often desert us. The current tariff turmoil is a perfect opportunity to make some very bad decisions. To help avoid this, here are some dos and don’ts for investors:

– Don’t keep checking your portfolio.

– Don’t watch financial news.

– Don’t think you will make good investment decisions in this environment.

– Don’t make emotional choices – sleep on it.

– Don’t listen to people who didn’t predict the current market tumult, when they predict what is coming next.

– Don’t listen to anyone predicting anything.

– Do focus on your long-term investing goals.

– Do remind yourself that equity markets have generated strong long-term returns despite frequent periods of losses (which are sometimes severe and we cannot avoid).

– Do remember that equity market losses always come alongside some very worrying news about the future.

– Do remember that nobody knows what will happen next – it might get better, it might get worse.

– Do remember that this is why you hold a diversified portfolio and have a long-term time horizon.

– Do go for a nice walk in the fresh air.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Uncategorized

The Two Most Dangerous Words in Investing

For anyone interested in investor behaviour, extremes matter. When there is a severe dislocation between the value of an asset and its fundamental characteristics, or spells of dramatic price performance, it suggests that some of the most powerful aspects of group psychology are taking hold. Such situations create both significant risks and opportunities. The problem is that identifying extremes is much harder than it seems. There are, however, a couple of words than can help – ‘always’ and ‘never’.

Market extremes are obvious, but unfortunately only obvious after the event. Once the extreme has been extinguished, we can happily carry out a post-mortem on the irrationality that led to it, typically ignoring the fact that for the extreme to have existed many people must have considered it to be justified at the time.

And, of course, this has to be the case. For market extremes to be reached there has to be a belief that the levels of exuberance or dismay surrounding a particular asset class is simply a sensible response to a changing world. The performance and persuasive narratives that accompany financial market extremes are taken not as the cause of it, but as evidence for its validity.

This creates a problem for investors. Periods of extremes are critical and come with major behavioural risks, but we struggle to identify or acknowledge them in the moment. What can we do about it?

As usual, there is a heuristic that can help. Perhaps the most reliable indicator that sections of financial markets are exhibiting extremes in sentiment or valuation is when investors start to use the words ‘always’ and ‘never’. The more we hear these uttered, the more we should pay attention.

The problem with the words ‘always’ and ‘never’ in an investing context is that they suggest a certainty that simply does not exist in the complex and chaotic world of financial markets.

Whenever we fall into the trap of saying something ‘always’ or ‘never’ happens, we can be sure that a performance pattern has persisted for so long that we have become unable to see anything else in the future: The US will always outperform”, “yields will never rise” etc…

‘Always’ and ‘never’ are reflections of two ingrained and influential investor behaviours – extrapolation and overconfidence. Prolonged trends often become perceived as inevitabilities.

At the point we have decided that nothing different can occur, valuations have undoubtedly already adjusted to erroneously reflect a level of certainty in inherently uncertain things.

Thinking in terms of ‘always’ and ‘never’ has profound consequences for investors, particularly in terms of how we build portfolios. The more certain we are about the future and the more confident we are in the prospects for a particular security or asset class, the less-well diversified we will be. Portfolios built on the idea that things ‘always’ happen or will ‘never’ happen are probably carrying too much risk. Market extremes inescapably encourage dangerous levels of concentration and hubris.

Of course there are things in financial markets that we can be more sure of than others. Saying that technology stocks ‘always’ outperform is very different to claiming that equity markets ‘always’ produce positive returns over the long-run. Neither of these statements are true, but one is inherently more problematic than the other.

What investors really need to be wary of is situations where there is an evident gap between the level of certainty we can possibly have in how the future will unfold, and the certainty with which we talk about it. When that gap is wide it ‘always’ ends badly.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Improving Earnings Do Not Mean a Rising Stock Price is ‘Justified’

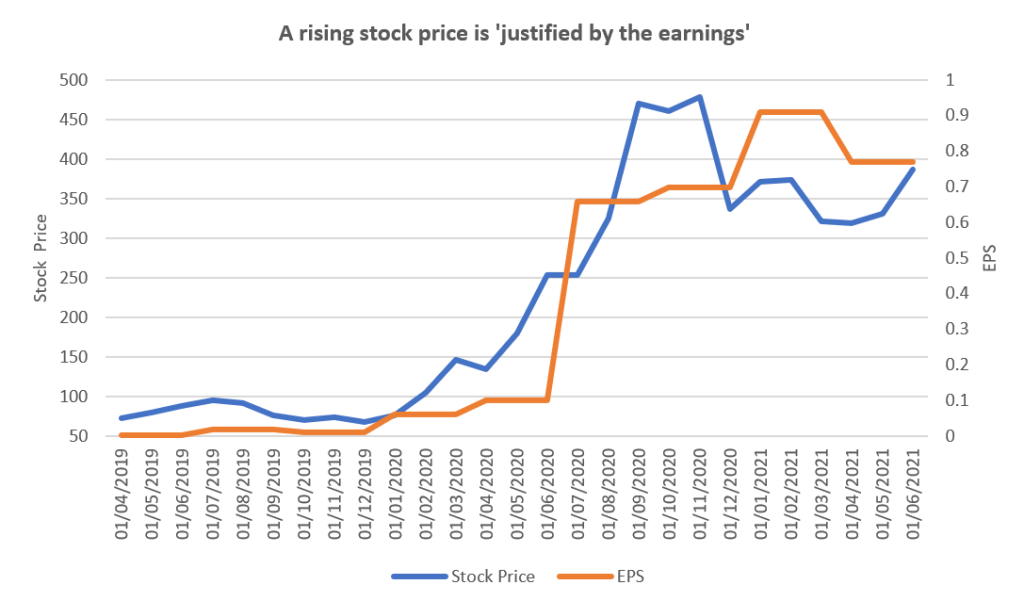

When a stock price has been enjoying a strong spell of performance it is increasingly common to see people argue that the move is ‘justified’ because earnings have been growing alongside it. The statement is usually accompanied by a chart a little something like this:

The point typically being made is that the company in question is not expensive because its increasing stock price is simply a reflection of improving fundamentals. This is a very simple and appealing notion, and also one which plays incredibly well visually. The problem is it can be exceptionally misleading as it ignores the critical variables that most long-term equity investors should care about.

Passing over the dual axis skulduggery which is so often apparent when these types of charts are presented, there are two major issues with making claims about the relationship between stock price performance and earnings growth:

1) Mixing the past with the future: EPS numbers are a reflection of the historic earnings of a company, while a stock price should (in theory) be based on expectations about the future earnings potential of a company. The only way that movements in EPS can ‘justify’ a current stock price is if it somehow affords us supreme confidence in the ongoing earnings prospects of that business. It may tell us a little, but it certainly does not give us a good answer to seemingly vital questions such as – how cyclical are the earnings of the business? What structural pressures might come to weigh on future profitability?

2) Ignoring valuations: The other glaring issue with such claims is that they seem to entirely ignore the valuation of the company in question. I appreciate that value has become a somewhat arcane topic but the earnings growth of a business surely has to be considered relative to its valuation. If we are attempting to assess the extent to which the EPS trajectory of a business is fairly reflected in its stock price movements, whether that business is valued on 5x earnings or 50x earnings feels like an important piece of information, but one which is often disregarded.

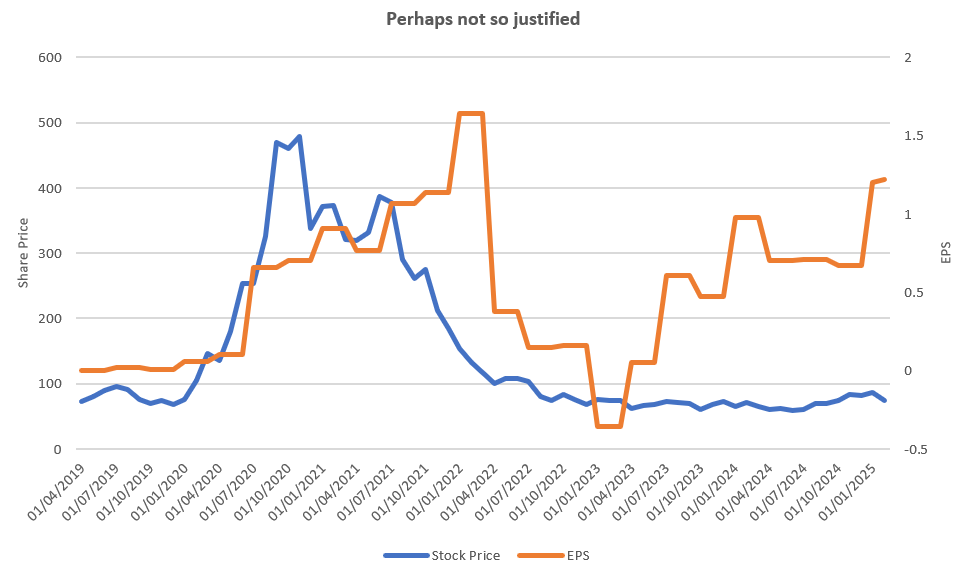

For a stock price to be fundamentally ‘justified’ in any way, we need to have a view on the valuation of a business relative to its future profitability. Observing a rising stock price and improving EPS really doesn’t help us answer such questions as much as many people seem to assume. Stock price moves can be justified by EPS moves, until they aren’t:

Although this type of comparison might not give us a great deal of information about the worth of a company, it does tell us a lot about the behaviour of investors and corporate management:

It’s all about earnings momentum: I have met many, many active equity investors in my career and I would say the most common approach is one based on earnings momentum; where the aim is to identify companies that are enjoying improving and consistently upgraded EPS. This is often not what is stated in their investment philosophy, but very apparent in their behaviour (there is a stigma attached to momentum investing and, unless you are a quant, nobody likes to admit they do it). The stock price to EPS chart is a simple representation of this type of momentum-driven activity.

This ubiquity of this type of investment approach is self-perpetuating. The more investors react to short-term earnings, the more stock prices react to short-term earnings and further encourage the behaviour. It is also a rational approach for many investors to adopt – if you have a time horizon of one or three years, then taking a momentum-orientated approach is likely the best survival strategy. Although you might care about the valuation of a business, by the time it starts to matter you may well be caring without a job.

Such momentum-led investors are as much, if not more, focused on how other investors will react to fundamental developments in the business, rather than the intrinsic merits of those developments to the business itself. There is nothing inherently wrong with such an approach, it is just different to being concerned about a company’s long-term value.

Corporate myopia: One of the consequences of the preponderance of momentum-orientated investors focused on short-term earnings developments is in executive behaviour. If positive stock price moves are increasingly the result of near-term EPS performance this will inevitably alter the decision making of management (on the assumption that their incentives are aligned with how the stock price performs). It seems reasonable to believe that there will be many occasions when a decision made with the objective of maximising short-term stock price performance is very different to one where the objective is long-term shareholder value maximisation. It would be nice if they were the same, but I seriously doubt they are.

The more short-term investors are, the more short-term management are. And so the cycle continues

The stock price of a company rising alongside its earnings really doesn’t help us understand whether it is justified or not, nor does it give us much indication about the long-term value of a business. Rather such comparisons tell us more about the type of investor we are.

* Charts comparing long-run equity market performance with earnings growth are fine. We should expect these to be closely related over time.

** To my mind, there are three types of active investors: Momentum, value and noise. Momentum investors care about price and are shorter-term. Value investors care about valuation and are longer term. Noise investors do random stuff and create opportunities for value and momentum investors.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

If Equity Markets Didn’t Fall as Much Their Returns Would be Lower

Perhaps it is the curse of frictionless trading and the rise of social media, or perhaps it is the unusually high returns delivered by global equities over the past decade, but investors seem more sensitive than ever to equity market declines. Even relatively minor ones like those experienced recently provoke dramatic responses.* At times such as these it is important not to lose sight of the fact that the returns from owning equities over the long run are as high as they are because they are volatile and suffer from intermittent drawdowns. We cannot have one without the other.

Starting with a very basic point – if we own a share of a company (hold equity), we carry the potential for a total loss of capital in the event that the business fails, and therefore we require adequate compensation for bearing that risk.

Thankfully, most investors are diversified across a large number of positions and are not entirely exposed to the fortunes of one company. We transfer the specific risk of part-ownership of a single business, to the broader market risk of holding a collection of them. This significantly reduces the range of outcomes we face – although we lose the potential for stratospheric returns from an individual holding, we also greatly diminish the prospect of disaster and complete failure.

This diversification benefit is an attractive trade-off for most investors, but although it limits one type of acute risk, it does not remove risk entirely. Even diversified equity exposure comes with risks and uncertainty that require compensation. This, however, is a feature not a bug – absent this uncertainty long-term returns would be significantly lower.

I tend to think about the risk to diversified equity investors as stemming from two types of uncertainty – short-term behavioural and long-term fundamental.

The short-term behavioural aspect is consistent with Thaler and Benartzi’s explanation of the ‘equity premium puzzle’. Investors are sharply sensitive to short-term losses and check their portfolios frequently. The daily fluctuations of equity prices create a huge amount of discomfort, which leads to poor behaviours, particularly during times of market or economic stress. The fact that this short-term volatility bears little relevance to the very long-term prospects of the asset class is largely irrelevant as – in the moment we experience it – it feels vital.

This creates a major advantage to investors with a long-term mindset (or the inability to check their portfolio valuations every day) but is far more difficult to capture in practice than in theory.

The long-term fundamental uncertainty element is simply that we cannot be sure what the results over time from equities will be. Although we can be confident that real returns from diversified exposure to equity markets will be positive if we hold them for twenty years – we don’t know whether this means 5% per year or 9%. Furthermore, we can never entirely discount the potential for very poor results from equities even over the long-run – the likelihood of this may be extremely low, but it is never zero.

These uncertainties combine to create high long run realised and expected returns for equities. If we were absolutely certain that equities would return 10% per year, then they would return a lot less than 10% per year.

There is a reward for bearing that uncertainty, but the catch is we do have to bear it. One of the biggest mistakes investors make is trying to capture the upside of equities while avoiding the downside. Given our dislike for even temporary losses this is entirely understandable, but incredibly dangerous, behaviour – one which is far more likely to act as a drag on performance than enhance it. The probability of us correctly anticipating and navigating each equity market drawdown (or prospect of one) is vanishingly small.

It is typically not the equity market declines that do long-term damage, it is the cost of the poor decisions we make during them. Such mistakes never come with just a one-off cost, they compound over time.

If we want to own equities for the long-term because we believe that they provide higher returns, it is important to understand why this is the case. Not only will this help us to manage the inevitably difficult times, but it will also allow us to shape our behaviour and time horizons to best capture those potentially high returns.

—

* Minor declines, so far. (18th March 2025)

–

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

New Decision Nerds Episode – Dealing with Trumpcertainty

Dealing with uncertainty is a constant challenge for investors, and now we are faced with a new and more dangerous variant – Trumpcertainty.

In the latest episode of Decision Nerds, we discuss the behavioural curse of uncertainty and how to cope in environments where it feels extreme.

We cover:

– Why uncertainty can feel worse than a loss.

– The evolutionary history of uncertainty aversion.

– How uncertainty impacts our behaviour.

– Why uncertainty acts as a decision making tax.

– How to communicate about uncertainty.

– What investors should and should not do in environments of heightened uncertainty.

The podcast is available in all of your favourite places, and here:

Dealing with Trumpcertainty

Trump Trades and European Equity Exceptionalism

An eternity ago (around four months), financial market commentary was dominated by confident predictions of the investment implications of Trump’s second term and countless descriptions of the inevitable performance advantage of US equities. Since this point, we have seen markets behave in an almost entirely contrary fashion to most of these forecasts (I don’t remember hearing many people call for the outperformance of Chinese and European equities). The problem is no matter how many times we get taught the same lesson about the futility and danger of such behaviour, we just cannot help ourselves.

One of the reasons that we perpetually repeat the same mistakes is that investors are incredibly adept at moving on from the things that we were thinking, saying and doing in the past (even if it is the very recent past) as soon as something else happens. While this does help us avoid coming to terms with the painful realisation of how little we know, it doesn’t help us make better future decisions.

About those ‘Trump trades’

Back in November I wrote that trying to forecast the market impact of the US election was a ‘wretched idea’. This was not due to the sheer unpredictability of Donald Trump, but because the global economy and financial markets are unfathomably complex systems and trying to anticipate them is impossible with any degree of confidence or accuracy.

The very notion that there is a straightforward relationship between a binary event (such as an election) and a financial market reaction (a strengthening dollar) is absurd. There may be self-perpetuating short-term reactions to such occurrences – investors trade based on what they think other investors will do – but, after this, things get incredibly messy, very quickly. Complex systems – like economies – are defined by being comprised of many component parts that interact with eachother, often in entirely unforeseeable and chaotic ways.

The issue is not that some of the higher profile ‘Trump trades’ look wrong at the moment – nobody knows how markets will progress from here – but that this type of investment thinking is totally at odds with reality.

European equities – dead or alive?

It may be hard to believe now, but the general sentiment around European equities in 2024 was almost uniformly negative. The sluggish European economy was blighted by bureaucracy and regulation, and their financial markets would never allow for the growth of hugely profitable technology-orientated firms like the Magnificent 7 in the US. Why would anybody invest in a laggard like Europe?

Well, it only takes two months of outperformance for those narratives to change. Now investors are hastily checking that they have enough exposure to a reawakening European economy. So much for the US being the exceptional market.

The old and new arguments are both ridiculously overconfident. The idea of US exceptionalism became as exaggerated as the dramatic transformation of sentiment towards Europe.

Investor feelings and behaviour are overwhelming dominated by short-term performance and the stories we create to justify it; most strongly held investing beliefs can withstand about a quarter of underperformance. This is because we are obsessed with what is happening right now and can’t seem to shake the belief that whatever it is will continue.

The truth is nobody knows whether the recent upturn in fortunes from European equities represents a new trend; we could just as easily revert to the performance patterns that have defined the past decade and more.

The fact that we cannot see the future means that we should always be diversified, and that means holding assets that even we might have written off ourselves.

Defensive investing

One of the more remarkable features of recent market moves is the performance of the European defence stocks. The current fervour for this area is in stark contract to five years prior when investors seemed incredibly keen to add such names to ESG exclusions lists and remove them from portfolios.

I have no wish to opine on the rights and wrongs of removing defence companies from a portfolio, but the dramatic shift in sentiment is a useful reminder not only that the world changes, but how we feel about the world also develops through time. We are all prone to believe that the things we think and feel presently are unshakeable. This is not true, not only will the environment around us evolve, but our perspectives and opinions are likely to alter with it.

What we staunchly believe now, may be very different in five years’ time for a plethora of reasons. We should always ensure our decision making is not so dogmatic that it fails to reflect this possibility.

The other – perhaps unpalatable – point is that our investment preferences are (like everything else) impacted by returns. Exclusions that are driven by genuine values are not always immune performance pressure.

We still can’t predict catalysts

Amongst strong competition, ‘catalyst’ is one of my least favourite investing words. People spend an inordinate amount of time talking and thinking about catalysts, but in the vast majority of cases all they are doing is trying to predict changes in market sentiment. Which, as you may have guessed by now, I do not believe we can do.

Imagine that last year you had a constructive long-term view on European equities because you felt that they were attractively valued – someone would have inevitably said: “That’s great, but what is the catalyst?”

Would you have said:

“Well, I think Trump will be elected as US President and his actions will shake the global world order, this will leave Europeans doubting the reliability of their most powerful ally, which will lead them to loosen fiscal constraints and improve nominal GDP prospects, and this will provide a major boost to earnings and sentiment.”

This would have been incredible foresight and if anyone did predict this, I missed it when reading through the 2025 outlooks.

Investors see catalysts everywhere when they look at past performance, but most of the time these are just stories told to explain outcomes. Most developments in financial markets do not have individual catalysts but come about due to a confluence of factors. Even on the occasions where there is an obvious singular catalyst – it is typically only observable after the fact.

Performance always comes first, explanations second.

Didn’t know then, and don’t know now

There have been some surprising developments already this year, which might mean that investors are reining in their attempts to forecast the future. Unfortunately not. One of the most puzzling but inevitable investor reactions to being blindsided by market developments is to immediately start trying to predict what comes next.

We were wrong then, but we will be right now.

The quicker we accept all that we cannot know or foresee, the quicker we can make sensible investment decisions that reflect that frustrating but inevitable reality.

—

For investors it seems that being consistently wrong is far more comfortable than being uncertain. So, despite the early months of 2025 giving us yet another valuable lesson in what we shouldn’t be doing, we will no doubt carry on regardless.

–

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

The Crystal Ball Test

At the 1998 shareholder meeting for Berkshire Hathaway, Warren Buffett said: “We try to think about two things: things that are important and things that are knowable.” Although at first glance this comment can seem quite innocuous, it is an essential idea to understand if we are to successfully navigate the uncertainty and noise of financial markets. Investors are generally quite poor at defining what matters to them and why; and this is a problem which causes all sorts of decision-making challenges. There is, however, a quick way to get better at this – a crystal ball test.

Before describing the test, let’s reflect on what Buffett is getting at here. He is saying that for his investment approach there are only a select number of elements that will influence results over time and an even smaller number of this group that are knowable (or predictable) to any reasonable extent. That is where his focus is.

Of course, nothing is perfectly knowable, but there are some things that we can have a sufficient level of confidence in, and many others that are, if not random, pretty close to it. The are far more things in the latter group than the former and distinguishing between them is vital.

Before worrying about whether something is knowable, we need to define which factors we believe are important to the success of our investment. How do we do that? Let’s turn to the crystal ball.

We can ask ourselves, and other investors, this question:

“If you had a crystal ball and could see one piece of information in the future that would materially influence this investment view, what would it be?”

We can apply this question to any type of investment – whether it be about an individual stock, or a major asset allocation shift. It should quickly elicit what we think the most important factors are, and then we can judge if there is any chance of us predicting it without the aid of a crystal ball.

Let’s take an example. If I had to take a view on the performance of ten year treasuries over the next five years, what would I want to foresee using the crystal ball? It would be US inflation in five years’ time.

This tells you that – for me – inflation is the most important variable in determining the returns of ten year treasuries over the next five years. Unfortunately, I have no idea what the rate of inflation will be, which obviously will impact how much conviction I would ever take in a view on US treasuries.

We can also invert the crystal ball question to get to a similar answer by asking:

“If you knew the outcome of X in advance, how would it impact your decision?”

If I knew the rate of inflation in the US would be 6% in five years’ time, it would almost certainly influence my view on US treasuries.

This type of question can help us cut short situations where people are debating some financial market issue that is not only unknowable but, even if we could predict it, we wouldn’t know what to do about it. (Elections are the gift that keeps on giving in this regard).

Using Buffett’s important and knowable framing, we can think about the usefulness of a crystal ball in three different ways:

– Something is both important and knowable: A crystal ball might help a little, but not much because we are reasonably confident in the variable anyway. (Think here of things like long-run earnings growth or starting valuations).

– Something is important and not knowable: A crystal ball is absolutely vital because something matters but we cannot anticipate it.

– Something is not important and not knowable: We can use the crystal ball as a paperweight because even seeing the future is of no use to us.

Unfortunately, investors are prone to spending far too much time in the latter two groups. Either making decisions that are heavily influenced by variables that are inherently unknowable, or wasting time on things that wouldn’t be useful even if they were knowable (which they aren’t).

The crystal ball test can be an exceptionally useful means of better understanding what type of investor we and others are. It is particularly effective in gauging what an investors’ true time horizon is (the factors that matter change with our horizon) and what variables are foremost in our thinking.

It is also a great sense check to stop ourselves spending an inordinate amount of time on financial market issues just because they are at the front of everyone’s mind, not because they are consequential.

How best can we incorporate Buffett’s thinking on focusing on what’s important and what is knowable into practice? I think there are seven key aspects. We should:

1) Be clear about the variables that are important to the success of our investment decision.

2) Understand whether these are sufficiently knowable / predictable.

3) Focus on elements that are both important and knowable.

4) Be aware of things that are important to our view but inherently unknowable.

5) Avoid high conviction investment views that are heavily reliant on unknowable variables.

6) Use diversification to protect against important but unknowable factors.

7) Stop worrying about things that are neither important nor knowable.

Investors are best served by adopting an approach where the most important determinants of success are also at least somewhat knowable. If we need a crystal ball for good outcomes, I don’t like our chances.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Dealing with Uncertainty

Humans hate uncertainty. The more uncertain we feel the more we take actions to restore a sense of control. For investors one inevitable response to increasing uncertainty is to make more predictions. If we can see the future, then we don’t need to worry about it. This creates the paradoxical situation where the harder predictions are to make, the more we want to make them.

In his fantastic book ‘Alchemy‘, Rory Sutherland gives an example of our aversion to uncertainty:

We are taking a flight to Frankfurt, which departure board would we prefer to see?

Option 1: BA 786 – Frankfurt- Delayed

Option 2: BA 786 – Frankfurt – Delayed 70 minutes

Although the delay in Option 2 is frustrating, it is far superior to Option 1 because it reduces the nagging discomfort of uncertainty. It gives us a little more confidence that the plane will actually take off and some idea of how much time we have. In Option 1, we know next to nothing and that causes considerable psychological pain.

In a similar fashion, Sutherland gives the example of the maps provided to show us where our Uber driver is. They don’t make the car get to us any faster, but they negate the uncertainty around when it will arrive. Investor predictions are a form of map making. They give us a guide to the future and, in theory, help to alleviate uncertainty. The problem is that financial markets are so chaotic and complex that the maps investors make are not much use.

It is possible to argue that hopelessly predicting our way through an uncertain environment is a good thing – if it makes us feel less anxious, maybe it is okay? I don’t think this is true. Investors holding a false sense of confidence about how the world will play out is likely to lead to worse decisions, not better.

Successful investing is about making choices that acknowledge uncertainty, not acting as if it can be avoided.

Our dislike of uncertainty makes selling certainty incredibly lucrative. We see it everywhere in the investment industry. Whether it is investment funds that claim they can navigate all environments with equanimity, or soothsayers selling investment forecasts. They prey on the pain of uncertainty by acting as if they are somehow prescient. (They are not).

Despite the discomfort that uncertainty causes investors, we do have a tendency to make things worse for ourselves. By engaging with markets too frequently we exacerbate our feelings of helplessness. We seem to believe that interacting with markets more will give us that elusive sense of control. Unfortunately it has the opposite effect. The more we immerse ourselves, the more likely we are to be captured by its ingrained unpredictability and amplify the behavioural risks we face.

There is no way to remove the uncertainty inherent in financial markets but we can adapt our behaviour to better deal with it.

The most important step is to value principles far more than predictions. A focus on sound investment principles such as diversification, long horizons and the power of compounding rather than inaccurate forecasts about an unpredictable future is essential.

Robust investment principles do not remove uncertainty (particularly over the short-term), but make us more resilient to it.

We also need to care about the right things. I have no idea what inflation will be in two years’ time nor what the Federal funds rate will be (nobody does), but I am reasonably confident that over the long-run economies will grow and that will flow through into corporate profits and stock market performance.

Nothing is certain but some things are more certain than others.

We all loathe uncertainty, but it is an inescapable feature of investing that we have to deal with. Our attempts to minimize it can lead to greater anxiety and poor judgements. Rather than seek illusory comfort from unreliable predictions or constantly redrawing useless maps, we are far better off accepting uncertainty and ensuring that the investment principles we hold are sufficiently robust that we have a chance of withstanding it.

That is the only way of being a little more certain of better long-run outcomes.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

The Perils of Line-Item Thinking

One of the key challenges faced by investors aiming to generate long-term returns with a diversified portfolio is ‘line-item thinking’. This is where we obsess over the success or failure of individual positions, often losing sight of our true investment goals and the principles of sound diversification. A good investment decision is not the same as a good portfolio decision.

Portfolio objectives are often framed in terms of beating a benchmark or ‘optimising’ for a given level of risk. Neither of these feels quite right. A benchmark-centric approach implicitly assumes that the benchmark is the correct base mix of assets for our requirements; while optimisations that are striving for ‘return maximisation’ within certain parameters suffer from inputting forecasts that we know will be wrong into a system very sensitive to those incorrect forecasts.

Rather I think for most individuals the objectives of our portfolios should be something along the lines of:

To maximise the probability of delivering good outcomes and minimise the probability of very bad outcomes.

It follows that any decision we make regarding our portfolio should be consistent with achieving those aims; and this is where the issue of line-item thinking arises.

What is line-item thinking? It is characterised by these types of behaviours:

– Thinking about the attractiveness of an investment on a standalone basis, or relative to one other asset. (I expect US equities to outperform emerging market equities, so I am overweight).

– Thinking about how an investment will perform in one future scenario. (I don’t think there will be a recession this year, so I prefer high yield to high grade credit).

– Thinking in terms of profit and loss, and whether an individual position ‘added value’. (This position detracted value and therefore was a mistake).

Although line-item thinking can seem reasonable in isolation, it is often antithetical to good portfolio decision making. None of the three examples above really help me achieve my portfolio objectives as described; they may even hinder it.

Positive portfolio decisions can often seem like bad line-item decisions.

Portfolio Neglect

The principal reason we build portfolios that combine different assets, funds and securities is diversification. The future is unknowable and therefore we want to create a combination of holdings that is resilient to that uncertainty. If we could predict the future, then we would only hold one security in our portfolio.

This brings us to the central behavioural challenge of diversification. Proof of it being effective comes in the form of assets and positions performing poorly (certainly relative to other things that we hold), but we have little appetite for owning stragglers.

Good diversification is about making choices that we expect to work in a world that we don’t expect to happen.

Line-item thinking exacerbates this problem because instead of considering the role each holding plays in meeting the objectives of our diversified portfolio, we think about them independently – did this asset, fund or view outperform or not? It works in binary, deterministic terms.

It is always about outcome bias

Outcome bias (our propensity to judge the quality of a decision by results alone) is one of our most pernicious and powerful behavioural failings. We cannot resist assessing portfolio performance after the fact and judging how the different components have fared. The underperformers and idlers are classed as poor decisions that cause us anxiety, while the outperformers are evidence of sound judgement.

This perspective makes sense through a line-item lens, but it is entirely inconsistent with making sensible portfolio decisions. We can quite easily make choices where an individual position performs well, but fails both criteria of increasing the probability of good outcomes and minimising the probability of very bad outcomes (particularly when only observing short-run returns).

The central issue is that good portfolio decisions are designed to make us robust to a range of unpredictable future results; if we do this, by definition, a decent chunk of our portfolio will look ‘wrong’ with the benefit of hindsight.

Our portfolio performance assessments come once a single market or economic path has been charted. Diversification always feels like a cost because nothing seems uncertain through the rear view mirror. Line-item thinking comes to the fore here – we look at each position, assess its performance and probably focus on the ones that have struggled.

This seems reasonable but is a terrible idea from a portfolio perspective. But what is the alternative? There are three critical portfolio-thinking questions to ask about the performance of individual positions:

– Was the decision reasonable at the time it was made given what we knew?

– Has the asset behaved in a manner that was broadly consistent with expectations / or its role in the portfolio?

– Did the decision meet the criteria of increasing the probability of good outcomes and minimising the probability of very bad outcomes?

Of course, asking people to think less about outperformance / underperformance of any given position is an entirely futile exercise. What’s measured is what matters! But the more that we think in such a manner, the less likely we are to make decisions that are consistent with meeting our overall portfolio objectives.

Line-item thinking is everywhere. Not a year goes by when the last rites aren’t read for a particular type of asset that hasn’t performed well. Bonds, value investing, liquid alternatives, non-US equities…have all come into the crosshairs in recent times.

These types of claims make sense from a line-item perspective, few of them do from a portfolio one.

Line-Item Duty

Given that it is portfolio outcomes that matter to us, not the ‘success’ or ‘failure’ of any specific position, why is line-item thinking so prevalent? One undeniable reason is simply availability – we see the line items, so we care about each of them – but there is a deep irony here. We like to check that we are diversified by looking at all the underlying holdings in our portfolio (we don’t want to see just a single line in our valuation even if there is plenty of diversification underneath that); but when we can view each of the underlying positions, it inevitably makes us want to rid ourselves of the poor performers.

Our desire to find proof of diversification leads to behaviour where we become less diversified.

Line-item thinking is also easy. Easy to prove and easy to measure. Positions either work or they don’t, and we were either right about how things panned out or we were wrong. Even attempting to explain why we might be happy that certain positions looked to have performed disappointingly, or why a decision that looks like a poor one actually made a portfolio more likely to meet long-run objectives is likely to be met with scorn.

The consequences of line-item thinking

There are several significant and deleterious consequences of line-item thinking:

Increasing portfolio concentration: Removing the laggards and increasing exposure to the winners is an inevitable consequence of line-item thinking – we don’t want to hold positions that are underperforming, so we reduce diversification and concentrate on the things that we got ‘right’. We create portfolios for the known past, not an uncertain future.

Less portfolio resilience: Line-item thinking means that we focus on whether a position is likely to outperform / underperform, rather than consider the role it might play in making a portfolio more robust to certain outcomes. A position that performs very strongly in a future that has a 30% probability of occurring can be incredibly valuable, even if on 70% of occasions it will look like a failure (on a line-item basis).

Too much risk: Line-item thinking will perpetually bias us towards higher return / higher risk assets. If we have the choice between two assets – we are always likely to favour that with a higher return potential even if it carries more risk and is less diversifying, because from a line-item perspective it is more likely to outperform.

Too much trading: Over-trading is an inevitable consequence of line-item thinking as we continually trade in and out of assets as they go through their performance cycles. Not only will we trade too frequently, but we will also almost always do it at inopportune times: Why don’t we hold more of that asset that has outperformed everything else in the portfolio, has enjoyed huge tailwinds in recent years and is trading on stratospheric valuations?

—

The more we think about the standalone merits and performance of any given holding or ‘line-item’ in our portfolios, the less likely we are to make sensible, well-calibrated decisions and be appropriately diversified for an uncertain future.

–

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

When the Incentives Change, I Change My Mind

The supine support offered to the new US President by multiple technology billionaires may be frustrating to some people but should be a surprise to nobody. They are responding to incentives, and incentives, more than anything else, drive behaviour. Our desire to understand and map the intricacies of human activity can sometimes lead us to overlook this inescapable truth.

In his wonderful talk: ‘The Psychology of Human Misjudgement’, Charlie Munger states:

“I think I’ve been in the top five percent of my age cohort almost all my adult life in understanding the power of incentives, and yet I’ve always underestimated that power.”

Humans are, of course, wonderfully complex, intricate and often irrational beings, but in some ways we are simple and predictable – particularly when it comes to incentives. If we had to anticipate the behaviour of an individual or group, the one thing we would want to know, far more than anything else, is the incentives at play.

This raises the question – but what incentives? We can be motivated and incentivised by many things, but if we start with money and power (and everything related to those aspects) we are probably on safe ground.

Despite the importance of incentives, it still feels like a neglected subject. Corporations spend vast amounts of money and time trying to understand individual and team behaviour, with barely a passing reference to the thing that is inevitably driving most of it – incentives.

One of the central reasons that big groups struggle to make good decisions or large companies become woefully inefficient is because with size comes increasingly divergent and misaligned incentives.

Misplaced incentives can have a profound impact on society. The seeming inability of corporations and governments to favour long-term thinking over the prospect of short-term wins is largely an incentive problem. Neither the CEO focused on the market reaction to their company’s next set of results, nor the politician two years away from re-election have incentives that encourage taking a longer-term perspective.

If incentives are so important to our behaviour, why do we so often ignore their influence? An undoubted issue is that few of us are willing to admit that our choices are driven by such brazen and base things. We almost always cloak behaviour driven by incentives into some more fulsome and thoughtful justification to make it palatable – both to other people and ourselves.

A key element of behaviour change is shifting incentives. If we observe divergent behaviour then we should immediately check whether the incentives have altered. While if we want to promote new behaviours then incentives are the most effective place to begin.

The first question we should ask when we are considering anything to do with behaviour or decision-making is – how are people incentivised? The answer will explain a lot.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).