The supine support offered to the new US President by multiple technology billionaires may be frustrating to some people but should be a surprise to nobody. They are responding to incentives, and incentives, more than anything else, drive behaviour. Our desire to understand and map the intricacies of human activity can sometimes lead us to overlook this inescapable truth.

In his wonderful talk: ‘The Psychology of Human Misjudgement’, Charlie Munger states:

“I think I’ve been in the top five percent of my age cohort almost all my adult life in understanding the power of incentives, and yet I’ve always underestimated that power.”

Humans are, of course, wonderfully complex, intricate and often irrational beings, but in some ways we are simple and predictable – particularly when it comes to incentives. If we had to anticipate the behaviour of an individual or group, the one thing we would want to know, far more than anything else, is the incentives at play.

This raises the question – but what incentives? We can be motivated and incentivised by many things, but if we start with money and power (and everything related to those aspects) we are probably on safe ground.

Despite the importance of incentives, it still feels like a neglected subject. Corporations spend vast amounts of money and time trying to understand individual and team behaviour, with barely a passing reference to the thing that is inevitably driving most of it – incentives.

One of the central reasons that big groups struggle to make good decisions or large companies become woefully inefficient is because with size comes increasingly divergent and misaligned incentives.

Misplaced incentives can have a profound impact on society. The seeming inability of corporations and governments to favour long-term thinking over the prospect of short-term wins is largely an incentive problem. Neither the CEO focused on the market reaction to their company’s next set of results, nor the politician two years away from re-election have incentives that encourage taking a longer-term perspective.

If incentives are so important to our behaviour, why do we so often ignore their influence? An undoubted issue is that few of us are willing to admit that our choices are driven by such brazen and base things. We almost always cloak behaviour driven by incentives into some more fulsome and thoughtful justification to make it palatable – both to other people and ourselves.

A key element of behaviour change is shifting incentives. If we observe divergent behaviour then we should immediately check whether the incentives have altered. While if we want to promote new behaviours then incentives are the most effective place to begin.

The first question we should ask when we are considering anything to do with behaviour or decision-making is – how are people incentivised? The answer will explain a lot.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Right Here, Right Now

Last week, I asked ChatGPT the following question: “Between 2018 and today, can you tell me what the major financial market worry was for each quarter?” Here was the response:

Reading through them all made me a little misty eyed about all the time spent in my career working on and worrying about issues that didn’t end up mattering that much (from an investment perspective, at least).

There is, however, a genuine problem here for investors. Financial markets tend to be an unstoppable conveyor belt of in-the-moment critical concerns that we cannot help but engage with, almost always in ways that are to our detriment.

It is human nature to be drawn towards things that are both salient and available. In financial markets, that means the more available (or prominent) an issue is, the more likely we are hugely overstate both its importance and the risk it presents.

Our engagement with this phenomenon typically works something like this:

Stage 1: A news story becomes the focus of investor / market attention.

Stage 2: We greatly overweight its long-term importance.

Stage 3: We develop ‘shallow expertise’ and a passable opinion on the subject.

Stage 4: We calculate our ‘exposure’ to the issue.

Stage 5: We inaccurately predict how financial markets will be impacted.

Stage 6: We either make a poor decision or have to justify not making one.

Stage 7: We move on to next in-the-spotlight news story.

Stage 8: We entirely forget what we said in Stage 1-6 within a few months.

For any investor with a reasonably long time horizon, attempting to ignore whatever the market is focusing on at any given point in time is the sensible (and most lucrative) approach. Unfortunately, this can be close to impossible. For three reasons:

– It is hard to ignore something when everyone else is paying attention to it.

– We are human and thereby exposed to the same risk perception biases as everyone else. We must work exceptionally hard to behave differently.

– Sometimes something will matter to financial markets in a material way and ignoring it won’t look smart.

The issue of something ‘mattering’ is an important one. Most high-profile stories will move financial markets in some way, but that does not mean it should be important to us. It should only really matter to us if it has a predictable, fundamental impact on how we are invested over a time horizon that is relevant. For most sensibly diversified investors this should be an incredibly high hurdle.

If we are obsessing over short-term market fluctuations, it is critical to remember that these are predominantly the activities of investors with entirely different objectives to those that we have. They are talking a different language, one that we don’t need to be conversant in.

One way to help protect ourselves from being frequently dragged into the latest financial market fascination is to keep a log of what it is we are worrying about each month and what we think about it. Looking back on how often seemingly essential topics fade from view might just give us a slim hope of insulating ourselves in the future.

What has our gripped attention right now will probably matter just as much as that financial market fixation from last month and the one that arises next month. I can’t wait to find out what it is.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

New Decision Nerds Episode – Room 101: The Downside of Investment Technology

In the latest episode of the Decision Nerds podcast, Paul and I discuss my final entry into the oblivion of Room 101 – investment technology. Choice, transparency and control are wonderful things for investors, but having the ability to react to every piece of financial market noise is a potential behavioural disaster with huge ramifications for our long-term returns.

We discuss why technological developments can facilitate bad behaviours, why nobody seems to care and what we can do about it.

The third of three short episodes is linked here and on all your usual podcast platforms.

Investing is Hard

Imagine it’s ten years ago and you are assessing the relative merits of market cap weighted exposure to US equities and an equally weighted allocation. Across a range of valuation metrics you can see that the equal weighted index is moderately cheaper. As luck would have it you also have a crystal ball that tells you that EPS growth will be greater for the equal weighted index over the next ten years. Same constituents, lower valuations and superior growth, that seems to be a great starting point for an equal weighted approach. So, what happened next?

Over the subsequent ten years the market cap index outperformed by close to 80%.

Investing is hard, and for many reasons:

Sensible decisions will frequently make us look stupid: It is not just that virtually all good long-term decisions will go through difficult spells; it is that seemingly prudent choices will often have negative outcomes and make us appear foolish.

Crystal balls aren’t enough: One of the inherent challenges of investment decision making is that the future is profoundly complex and uncertain. Our conviction must always be tempered by the vast amount we cannot and do not know. As the equal weight US equity example shows – even a glimpse of the future will often not be enough.

Sentiment can overwhelm everything: It is not just that it is hard to forecast future fundamentals, it is that anticipating fluctuations in sentiment is even more challenging. The underperformance of equal weighted US equities over the past decade has been driven by a transformation in the perceived prospects of the largest companies in the market.

A longer time horizon doesn’t guarantee success: Having a long time horizon is the greatest advantage any investor can have. (How long? As long as possible). Unfortunately, it is not enough to ensure a positive outcome. Although the impact of swings in sentiment fade with the passage of time, they can still exert a huge influence over periods longer than most of us can bear. A long-term mindset is still our best chance of success. It materially improves the odds, it just doesn’t provide anything close to certainty.

Extremes matter: The psychology that drives financial markets means that prices tend to traverse periods of unbridled optimism and entrenched pessimism. Assets don’t always rest in an equilibrium state. This means that active views are probably best taken when those extremes are already evident – leaning against excesses is probably where the probability of success is greatest. Marginal active views (like equal weight versus market cap ten years ago) are too often beholden to the next unpredictable shift in sentiment.

–

It is somewhat dispiriting to know that even if we had advance knowledge of critical equity market fundamentals, we would still likely look as if we had made an irrational decision. There are vital lessons that stem from this example, however. Most importantly that humility is the critical trait for all investors – we will frequently be wrong, and our actions and behaviour should reflect that. What is the best evidence of a well-calibrated, humble investor? Sensible diversification.

Investing is hard and the future is uncertain. It should show in our portfolios.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

New Decision Nerds Episode – Room 101: Performance Fees

My first nomination for the Decision Nerds podcast Room 101 was a relatively gentle chart crime; my next investment industry pet hate to send into oblivion might be a little more controversial – it’s mutual fund performance fees.

What’s my problem? Well, such fee structures are often framed as better aligning client interests and fund manager incentives, when often they do no such thing. Rather they create a ‘heads I win, tails you lose’ asymmetry and one that is not (surprise, surprise) in the interests of the client.

You can find out a little more about my thinking, why Paul might disagree and how fees can be better structured.

The second of three short episodes is linked here and on all your usual podcast platforms.

It Was the Best of Times, It Was the Worst of Times (to be an investor)

There has never been a better time to be an investor. We have unprecedented choice, transparency and control. There has also never been a worse time to be an investor. We have unprecedented choice, transparency and control.

Although it may seem heretical, there is a strong case to be made that the evolution of the investment industry – in particular the wonderful technological advancements – has actually made life more difficult. Why? Because so little thought is given to the behavioural consequences of the profound changes we have witnessed. Indeed much of the technological progress we have seen threatens to turn investors into gamblers.

There are two elements that are central to short-term investor decision making – emotional stimulus and friction.

Emotional stimulus simply means that how we feel impacts and often overwhelms the choices we make. What the psychologist Paul Slovic might call the ‘affect heuristic’.

This could be fear, greed, anxiety, excitement, envy or a multitude of other things. The problem for investors is that we are engulfed by a constant barrage of financial market babble that inevitably provokes an emotional response. We can see how our portfolio performs minute by minute, we hear about the incredible successes of other investors on social media, we get bombarded with news about every market fluctuation. All of these things make us feel something, which often compels us to take action.

This might be harmless enough if it were it not coupled with another development – the removal of friction from our investment decision making.

Friction simply means how hard something is to do, and it is more powerful than we think. As Robert I. Sutton and Huggy Rao argue in their new book: ‘The Friction Project‘, we can get ourselves into big trouble by making the wrong things easy and the right things hard.

The issue for investors is that technological developments have made many things easy – checking portfolios and trading – but without careful consideration of the negative behavioural implications. Investors have ended up in a situation where we are overwhelmed by emotional stimulus and have no friction to stop ourselves reacting to it.

It is as if the industry has said – ‘humans are prone to costly behavioural mistakes, so let’s make them as easy as possible to make’.

Of course, it is hard for any investment provider to say to their clients – ‘we are going to make things harder for you because we don’t trust you to make sensible choices’, but at the very least stronger behavioural interventions and better guidance is a necessity.

In the UK, online gambling firms are subject to a range of requirements related to client behaviour in order to obtain a license. Tools such as deposit limits and time outs are required features. These act as behavioural checks and balances, imperfect certainly but at least acknowledging some of the unfortunate realities of human behaviour.

It is easy to say that investing and gambling are two different things, but they are not so distinct from eachother. Indeed, the exact same decision may be a gamble for one person and an investment for another.

Two people might buy the same amount of Apple shares, one for a long-term share of profits and the other because they think the company will beat earnings forecasts later that day. One decision feels like an investment and the other a gamble. The difference between the two can sometimes just be intent and opportunity.

The present environment for investors – defined by noise, emotional stimulus and an absence of friction – will almost certainly drag many of us away from investing and towards gambling, where our actions will be increasingly short-term and speculative with poor odds of success. This is in the interests of some in the industry but certainly not most investors.

This frictionless backdrop also makes how firms communicate more critical than ever. Flooding investors with incessant market comment might be okay if there is friction present. If it is hard to trade, then maybe what is said doesn’t really matter as it is all quickly forgotten. This doesn’t apply anymore. Anything that is communicated to investors might be acted upon. Nothing should be considered benign. We should always ask – how might what we are saying make an investor feel and what might they do about it?

I understand the theory about why today is such a fantastic time to be an investor and much of it is valid. I fear, however, that human nature might mean there has never been a worse or more dangerous time to be an investor.

It is probably time we took behaviour seriously.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

New Decision Nerds Episode – Room 101: Chart Crimes

A new year is a time of hope and optimism, and also an opportunity for me to complain about some of my investment industry pet hates. In the latest episode of the Decision Nerds podcast, Paul Richards and I open the door to Room 101, where I get to send some of my least favourite things in asset management into oblivion.

Room 101 is the torture chamber in George Orwell’s classic book, ‘1984’; for those who cross its threshold, it contains, ‘the worst thing in the world’. In Britain, Room 101 became a popular TV and radio show where celebrities suggested things to be consigned into the dreaded room.

Crimes of the charting kind.

I somehow managed to whittle my list down to three and the first episode kicks off with a seemingly minor but pervasive peeve – chart crimes, in particular those charts where a current time series of a financial market metric is overlaid with one from a different period of history. The current favourite of this genre is the path of inflation now compared to the 1970s/80s.

Wonderfully compelling, but total nonsense.

Rather than just hear my gripes, Paul tries to get to the bottom of what it is about this type of ‘information’ that I really don’t like.

The first of three short episodes is linked here and on all your usual platforms.

What Do Investors Expect in 2025?

As you may have gathered by now, I am a little sceptical of financial market forecasts. That does not mean, however, that the formation of expectations is not a fascinating subject. Towards the end of 2024 I ran a survey of 276 finance professionals to uncover their thoughts on the year ahead.

I posed ten questions, and here is how they responded:

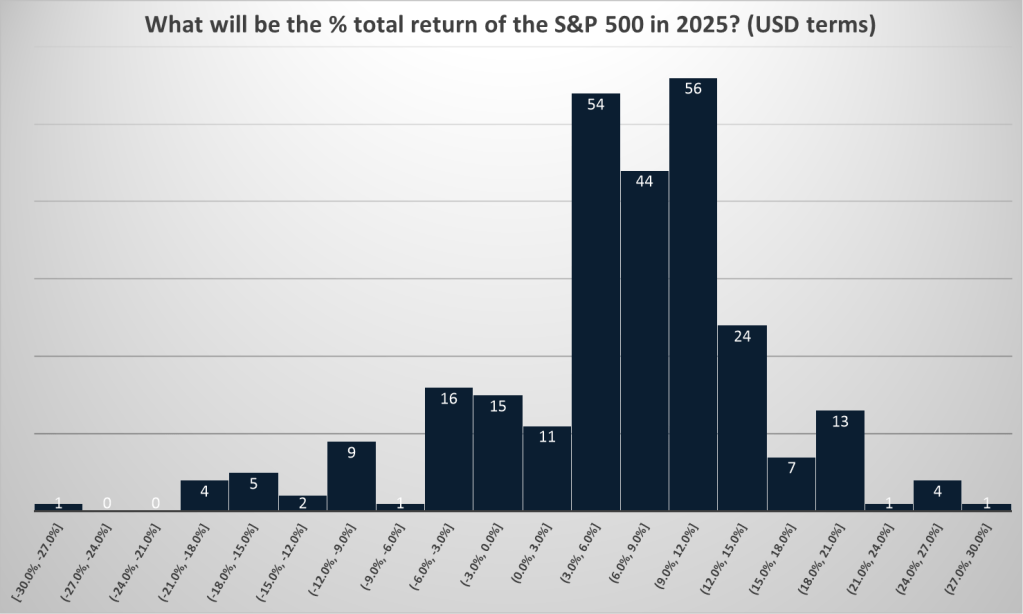

Question 1 – US Equity Market Returns

Expectations are for a positive but more subdued 12 months for US equities with a mean return of 6.5% and median of 7.0%. Although these seem quite prudent predictions, and broadly consistent with long-run equity returns, performance of this nature has become quite unusual. Since 1965 calendar year returns for the US market above 27% are more common (12) than returns between 3% and 12% (11).

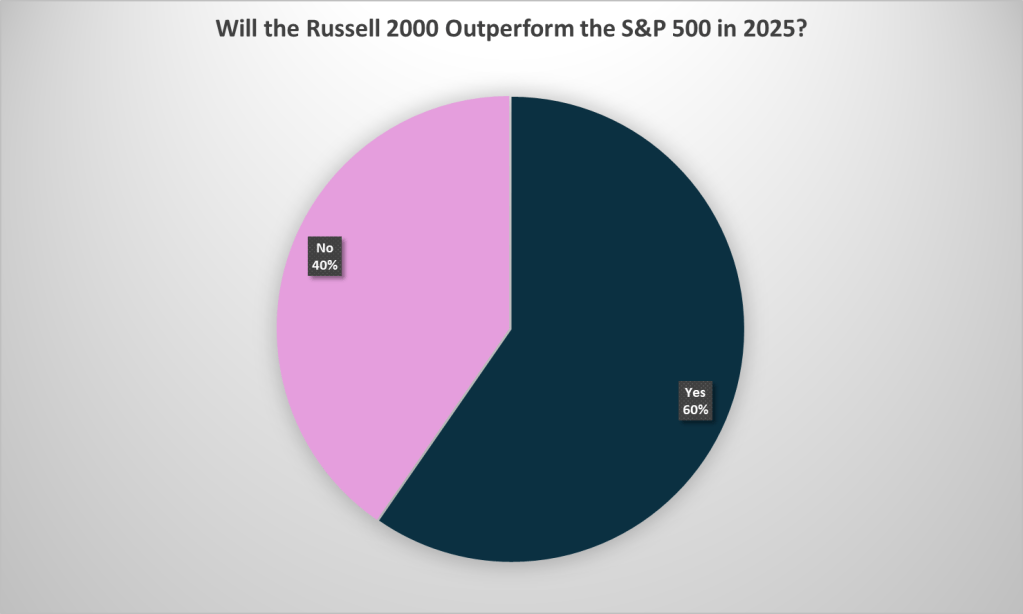

Question 2 – Small Cap Revival

Hopes abound for a resurgence in US smaller companies, which have been out of favour for a considerable period of time. Since 1979 the Russell 2000 has outperformed the S&P 500 in 48% of calendar years, but has trailed its larger counterpart in eight of the last 10.

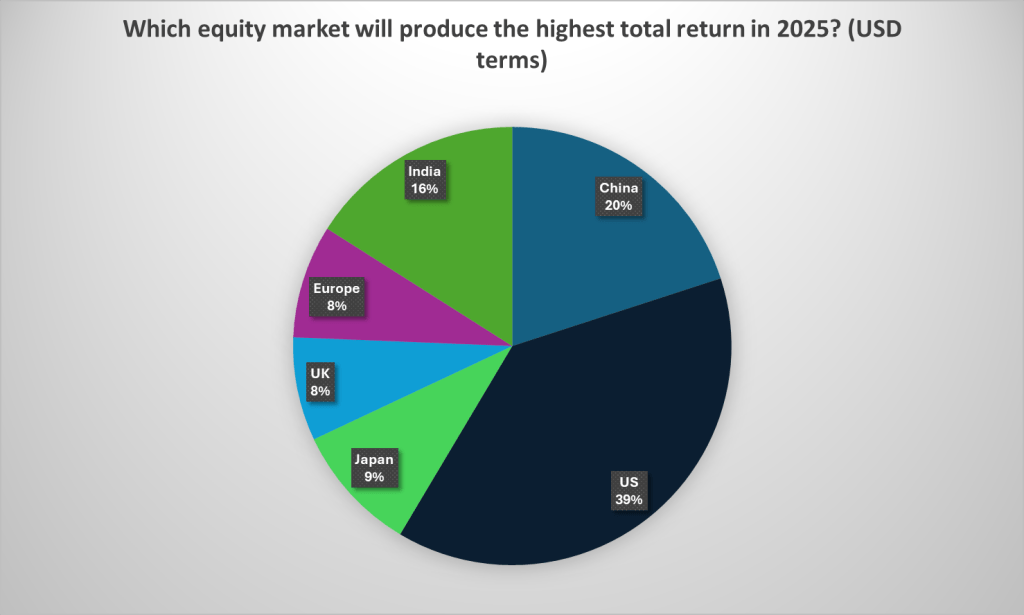

Question 3 – US Exceptionalism

Although confidence in the continuation of US equity outperformance is unsurprising, it is hedged (at least a little) with some contrarian, value calls on a Chinese recovery. UK, Europe and Japan remain in the doldrums.

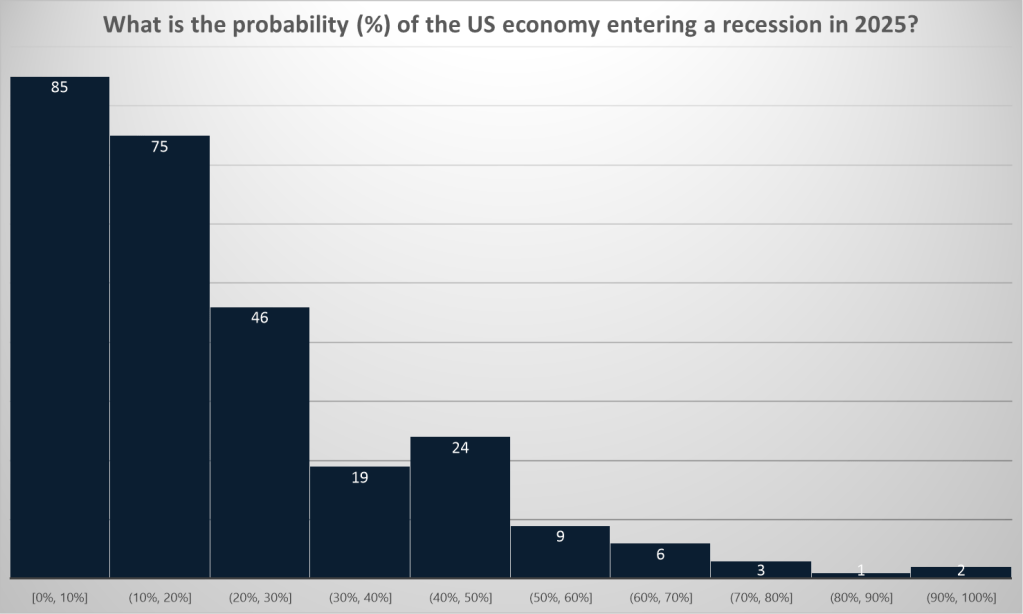

Question 4: Recession Risk

Recessions are notoriously hard to predict, most experts struggle to do it even when we are in one. The mean response in the survey is 25% (20% median), so not far off broad market consensus. But beware, in 2022 there were reports of a 100% chance that the US economy would enter a recession over the next 12 months. (Never forget Cromwell’s rule).

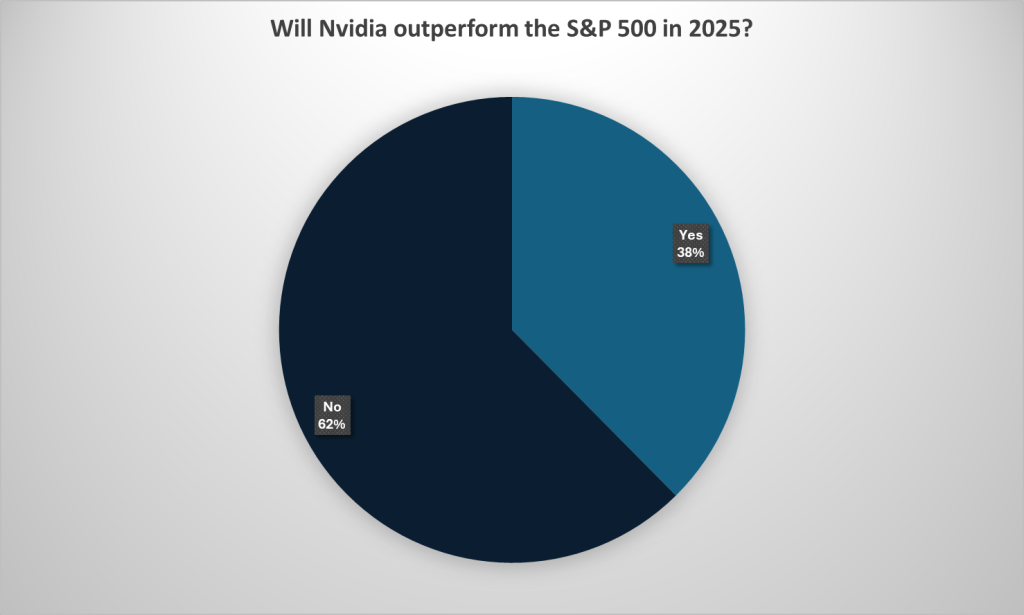

Question 5: The Magnificent 1

Given the respondents’ confidence in continued US equity outperformance, that 62% expect Nvidia to underperform the market is somewhat surprising. Allied with a positive view on the Russell 2000, there are perhaps hopes of a broadening out of returns – maybe it will be the fabled ‘stock picker’s market’!

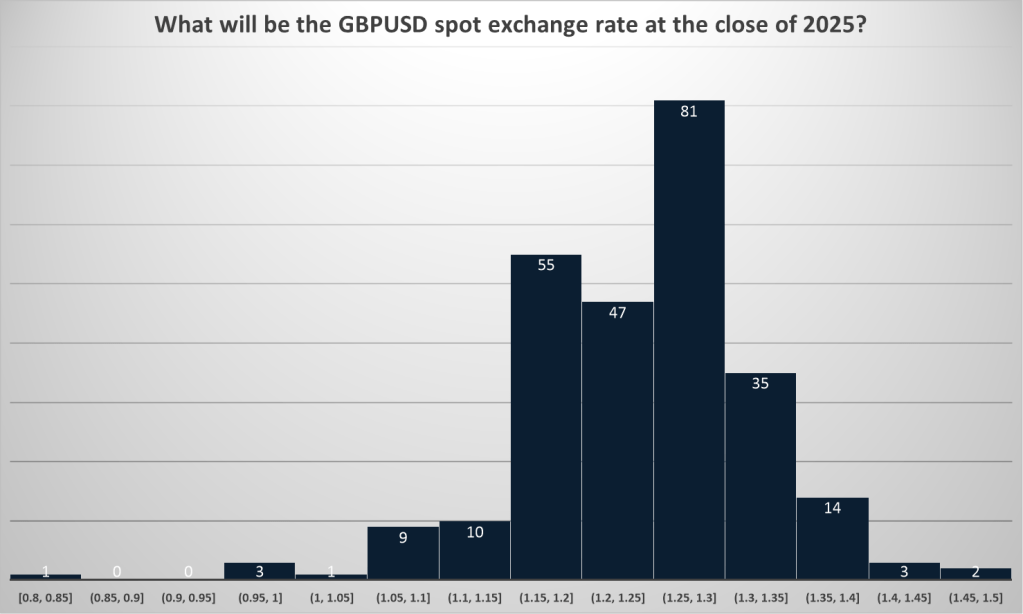

Question 6: Dollar Dominance

All financial market forecasting is difficult, but currencies are undoubtedly amongst the toughest. Although many variables will impact exchange rates they are heavily influenced by inflation dynamics and interest rates – two other things people cannot predict. Reassuringly, expectations here are pretty conservative with a mean GBP:USD of 1.26.

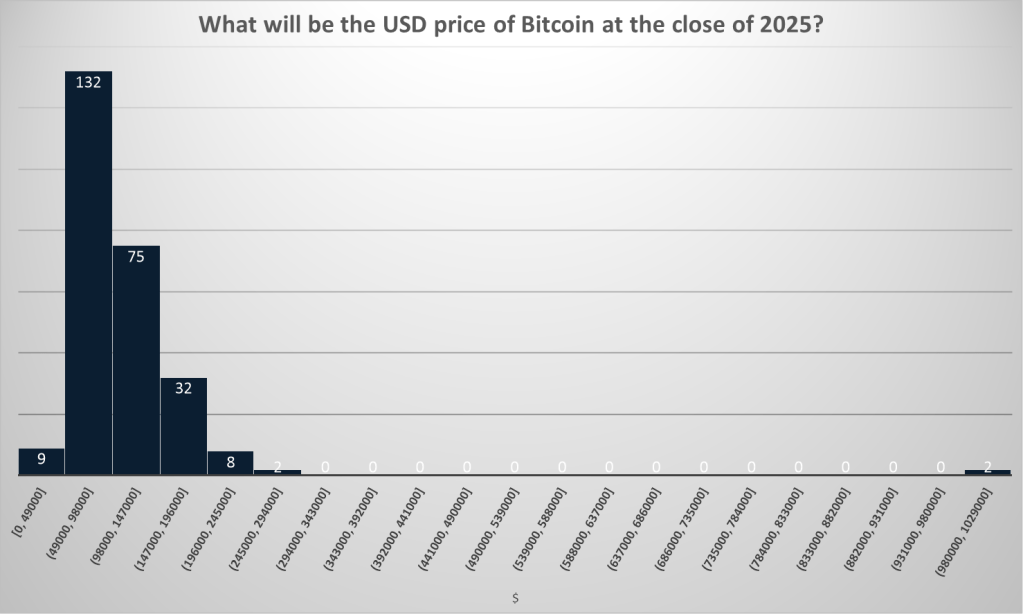

Question 7: Bitcoin

How to predict the ultimate bubble / belief asset? Who knows? This is probably the question where the sample most markedly impacted the answers – a different group of people would likely had wildly divergent expectations. The general mood in this survey was negative with a mode of $50,000 and a median of $95,000. The mean, however, was aided by a couple of $1m predictions.

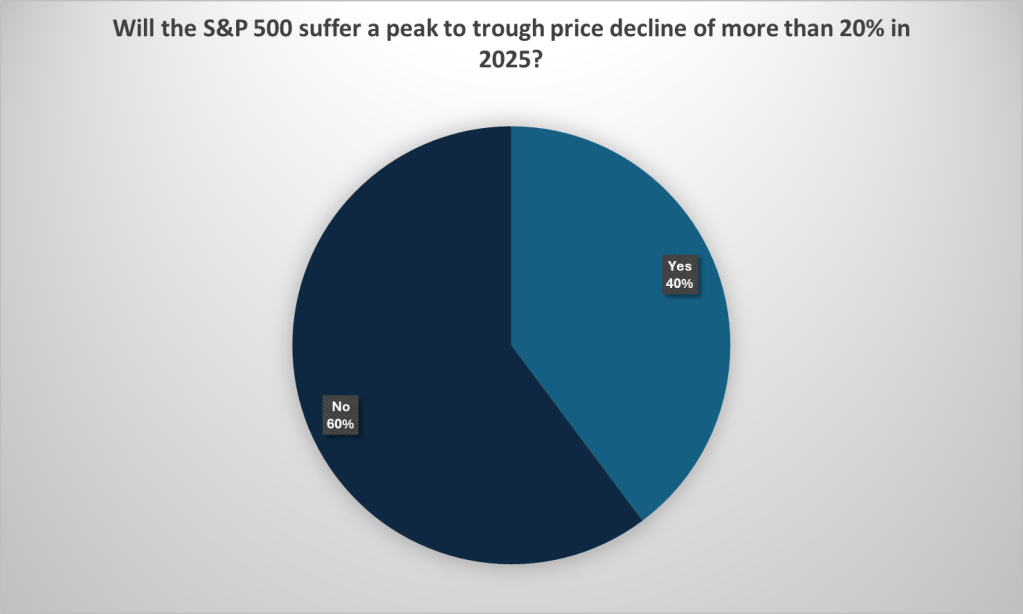

Question 8: Bear Market Risk

20% declines in US equities (the classic definition of a bear market) are pretty rare – somewhere around 15% chance in a 12 month period historically – so the 40% figure here is high, and may reflect concerns over valuations and concentration.

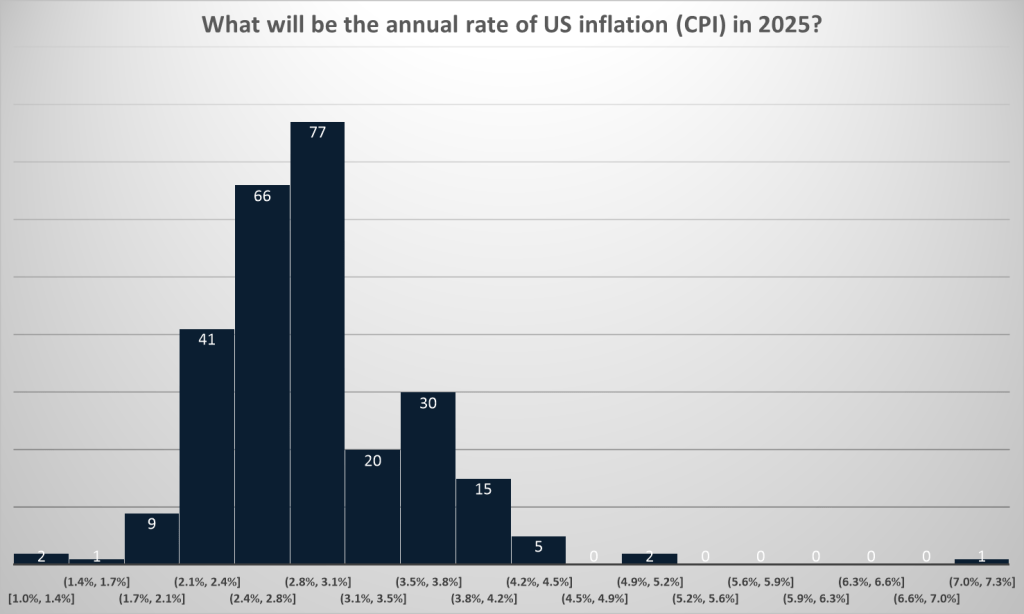

Question 9: US Inflation

Very few participants expect the Fed to hit their inflation target and inflation risks appear skewed to the upside – though not egregiously so. The median view was 2.9%.

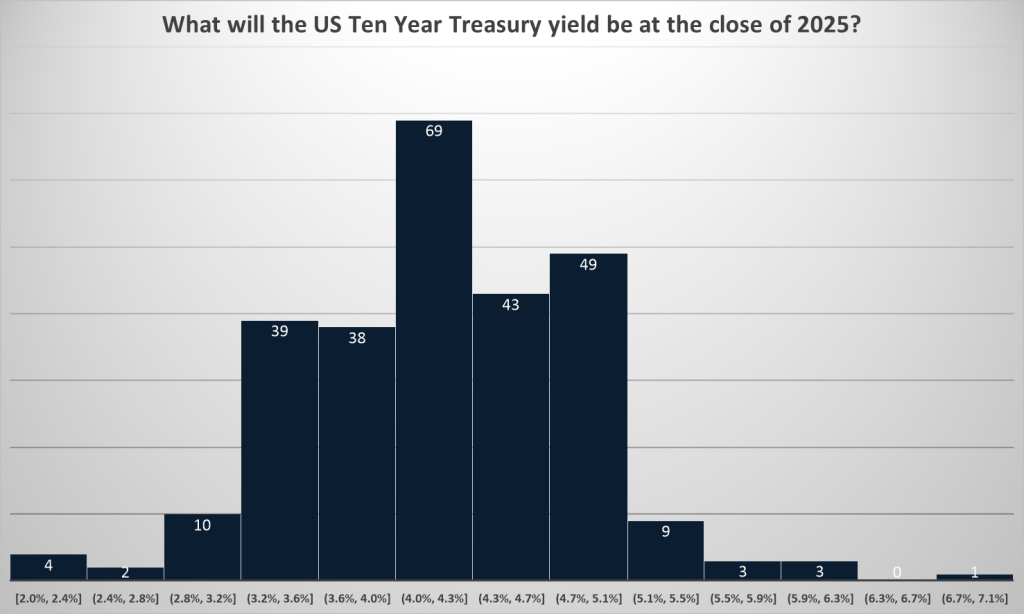

Question 10: US Treasuries

Despite all the talk of fiscal challenges and inflation risks, ten year treasury yield expectations seem well-anchored. The mean was 4.2%, slightly above a 4.1% median. 20% of respondents expect the yield to finish the year above 5%, compared to 34% below 4%.

_

Probably the most important part of this survey was the option for participants to receive a copy of their answers. In 12 months’ time when everything has changed we will have little hope of remembering what we were thinking and feeling about markets a year ago. This conscious or unconscious lack of ‘forecasting memory’, is one of the main reasons many of us can’t quit the habit of making investment decisions based on predictions we have little hope of getting more right than wrong. Forecasting should be for fun only!

I will be back this time next year to see how we did.

Thank you to those who participated.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

What Are Your Financial Market Expectations for 2025?

I am carrying out some behavioural research on financial market expectations for 2025 and have created a brief survey for people involved in the finance industry to complete.

The survey is very short and simple – it only has 10 questions so should take little more than two minutes of your time. It is also anonymous, so there will be no prizes for good predictions or censure for bad ones!

There is an option to have your responses emailed to you, so this time next year you can review how close your expectations were to reality. I will also follow up with some details on the distribution of market expectations across all respondents early in the New Year.

Thank you for your help.

Financial Market Expectations 2025

The Trouble with US Equity Exceptionalism

It is difficult to go a day without coming across another article explaining US equity exceptionalism. This is unsurprising given that performance has been outstanding both in terms of its magnitude and duration. Yet there is a concerning aspect with many of these pieces – rather than simply explain what might have caused exceptional returns from the US equity market, they almost always make the case for their persistence being inevitable. Whenever investors talk and behave as if the future is both obvious and unavoidable it is sensible to be wary – this time is no different.

Prolonged outperformance is always exceptional

The idea of exceptionalism is not unique to US equities, it is the same argument that is always made about an asset class that has delivered unusually high returns for a sustained period of time. Emerging market equities, dotcom stocks and Japanese equities have all enjoyed spells of being defined in such a way after prolonged and pronounced outperformance. This is driven by the tendency of humans to extrapolate both past returns and the stories which accompany them.

Duration is also an incredibly important factor. The longer such trends persist the harder it becomes to see anything else occurring in the future. Contrarians aren’t broken by the magnitude of poor performance they are broken by its length.

The core point of the exceptionalism claim (for any asset class) is that what has occurred is a secular, permanent feature of markets rather than some temporary phenomenon. Whenever an asset class enjoys exceptional returns for an extended period this argument must be made – it is essential to its continued success. Why? Because as investors are persuaded / compelled / forced to invest more in that asset the only way they can justify it is to make the exceptionalism case.

As a portfolio manager prepares to tell their Investment Committee that they are increasing their allocation to US equities they can hardly produce a PowerPoint slide saying that they are capitulating after significant performance pressure or that they are probably investing at the peak of a cycle. Rather they have to say that US equities are truly exceptional, and they now believe that the advantages are structural and will last in perpetuity.

This is not to say there is nothing exceptional about US equities (more on that later), but simply that the same type of stories justifying the same types of behaviour are always told around asset classes which deliver lengthy spells of uncharacteristically high returns.

If you are ever in doubt about why investors are making the decisions that they are – rest assured that the answer is almost always past performance.

What do we really mean by exceptional?

Asset class exceptionalism is always identified after the fact – but what does it mean to be exceptional?

Although often left undefined, when people talk of exceptionalism they are referring to features that afford an asset class the ability to deliver enduring outperformance. Its causes can be placed into three groups:

Structural: Permanent (or at least very long-term) aspects of an investment that proffer it a return advantage.

Cyclical: Factors that have a variable influence on an asset class’s returns – largely dependent on capital / economic cycle.

One-off / Singular: Exceptional returns for a period driven by a one-off confluence of variables within a complex system at a particular point in time – these are not permanent nor likely to be repeated.

Exceptional returns are almost always a convergence of these factors, but our tendency is to greatly overstate the role of structural drivers over cyclical phenomena. We are also liable to entirely ignore the influence of one-off factors.

Let’s take one version of the US equity exceptionalism justification. US markets are the most shareholder-friendly in the world, they allow for the emergence of large, significant and successful companies. The US is the market that allows more of the gains of capitalism to go to companies and the individuals that own them. (This may come at the expense of other elements of society, but that is not for this post).

This is a structural argument and one which – in broad terms – is very common. Is it true? Possibly. Does it lead to exceptional stock market returns? Maybe, but few people were saying so in 2010.

But what about the one-off argument? At the start of this exceptional run of performance the US equity market was in the relative doldrums so had undemanding valuations. This was combined with a wave of material technological developments that transformed the economic and financial market landscape and led to the full emergence of a range of staggeringly successful and sizable US listed companies. The financial magnitude of their successes allowed them to make gargantuan investments which further bolstered their dominance.

Here we have a mix of variables – some combination of situational luck and structural circumstance that fostered a pattern of returns that have led to great confidence in ongoing exceptionalism. Yet even if this explanation were to be right (it is not – it will be at best incomplete), it is difficult to ascertain how much of the high returns we have witnessed are to do with something ingrained in US markets and how much is due to the emergence of some exceptional tailwinds.

The answer is always a complex web of factors and nowhere near as simple as any explanation that we might find here.

What does US exceptionalism mean for future returns?

Exceptionalism is justification for past outperformance, but what does it mean for future returns? Continued strong returns is the simple answer, but that is not sufficient. If we ignore the short-term vagaries of sentiment, then claims about equity market exceptionalism must be about superior earnings growth. The central argument of US exceptionalism is that its earnings will grow faster than other markets (let’s ignore starting valuations for the moment). This has certainly been the case over the past decade, but is it set to persist indefinitely?

One of the challenges is where the earnings growth advantage has arisen in recent years – it has been dominated by the ‘Magnificent Seven’ stocks. Although the fundamental performance of these names has been (in aggregate) undeniably outstanding, there is an inherent challenge in the largest companies in the world delivering EPS growth north of 30% per annum if nominal GDP is somewhere around 5%. These two figures are likely to converge over time and I could hazard a guess in which direction. Of course, companies can also claim a greater share of overall growth (even if the rate of economic growth is modest) but this gets increasingly difficult at scale.

This is not to paint a negative outlook for these companies, but rather to make the point that continuing to deliver exceptional results gets harder from here (even ignoring what is already reflected in valuations).

The importance of the Magnificent Seven on the exceptional status of the US equity market also raises an important question. What exactly is it that makes the US exceptional? If it is a broad statement on the overall environment then we should expect equally impressive outcomes from small caps or an equally weighted version of the market. Or is it more that the US is a more fertile environment for the emergence of hyper-successful and sizeable companies? This distinction feels important.

What is the right price for an exceptional market?

At this point of a market cycle simply mentioning valuations can seem somewhat arcane and is often met with a roll of the eyes, yet even exceptionalism should have a price.

One of the comments I often hear is that the US has consistently outperformed despite being expensive ‘forever’, so valuations are clearly meaningless. This is not true – for much of its decade or more of outperformance the US equity market hovered around its long-run average valuation level relative to other global markets, it is only in more recent times where the valuation premium has reached extreme levels.

Saying that valuations are irrelevant makes no sense. They are a terrible timing tool and often an overly simplistic way of assessing return prospects, but that does not make them redundant.

Imagine that US equities come to trade at 100x cycle adjusted earnings and the rest of the world 25x – are valuations still a non-factor for future return expectations? I doubt it. If we believe that there is a return premium for US exceptionalism, we should also be willing to consider what we are comfortable paying for it. If we pay too much, we might not get a premium.

Let’s make it into a very simple question: Over a long-run horizon what earnings growth advantage do we expect a set of US listed companies with global revenue streams to hold over a set of non-US listed companies with global revenue streams?

If we can answer that then we should be able to think about what a reasonable price to pay for that advantage might be. I am not sure what the solution is, but it shouldn’t be that the price we pay doesn’t matter at all.

Everyone already behaves as if US equities are exceptional

One of the puzzling aspects of conversations around the US equity market at the current time is the notion that US exceptionalism is underappreciated. Let’s be clear here – the US equity market represents over 70% of globally equities. The next largest single country is around 5% (Japan). The fortunes of the majority of investors are inextricably tied to the future performance of the US equity market – both the continued outperformance of the market and investors actively growing their exposure increases this reliance. The size and valuation of the market is reflecting the belief that the US has been exceptional and will continue to be so.

Another behavioural oddity that the current situation of the US equity market is a fascination with minor relative positions over very large absolute positions. In simple terms – an investor with 68% of their portfolio invested in US equities will often seem to worry more about being 2% underweight than the 68% absolute allocation they hold in one market. Over time only one of these things will matter.

A profound challenge with increasing market dominance and concentration is that diversification becomes incredibly difficult. Not only does the outperforming asset (US equities in this instance) passively become a more prominent feature of most portfolios, but the development and reinforcement of the ‘exceptionalism’ narrative means that investors don’t want to be diversified – why would we? We just want to own the exceptional option.

—

Given the current fervour for US equities, this will no doubt be read as a bearish piece on the asset class – it is not – it is and should remain an important part of most portfolios. We should, however, always be cautious of situations where investor narratives and behaviours suggest the future is far more certain than it can possibly be.

–

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).