At the pinnacle of its bubble in 1989, a toxic combination of loose monetary policy, rampant loan growth and a spiralling cost of land led the Japanese equity market to trade at close to 100x cycle adjusted earnings. Inevitably this heralded decades of disastrous returns. Between 1990 and the end of 1999 the annualised return from Japanese equities was -4%; over the following decade it managed to fare even worse posting -5% returns per year.[i]

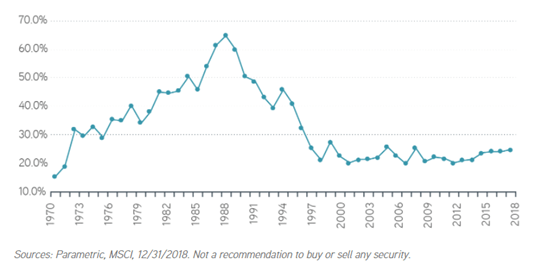

Although investing at such extreme prices seems foolhardy; passive global equity investors would have been increasingly exposed to Japan as the bubble inflated with their allocation hitting 45%. On an EAFE basis the concentration reached 65%:

Does this trait of growing exposure to astronomically priced assets mean a market cap based country allocation is a terrible idea?

No, it is perfectly rational. It just comes with costs and limitations. As with any investment strategy.

In this binary world our default view is to stridently take one side and vehemently oppose the other. Committed passive investors will claim that an active country allocation is non-sensical given the underwhelming performance history. Active management advocates will argue that any approach that ingrains objectively bad decisions – like allocating half of our assets to staggeringly expensive markets – runs counter to all evidence about what drives long-term returns.

Financial markets are just too noisy and uncertain to take such forthright and singular views. Often two statements can entirely contradict each other whilst both being true.

Take the below examples:

A passive, market cap approach to global equity investing has and will prove to be an effective long-term option for many investors.

and

Investing near half of our equity assets in a market trading at 100x cycle adjusted earnings is an awful strategy.

If we accept the evidence that buying very expensive assets is a recipe for poor future returns; how is it possible to claim that passive global equity investing can also be a sensible course of action?

There are several valid arguments a passive investor might make:

1) We do not believe there is another method that can consistently put the odds in our favour. It is not enough to say that a market cap, global equity allocation is deeply flawed; we need to have confidence in a robust alternative.

2) The long-run return of global equity markets incorporates incidents of bubbles and manias; they are a known and expected feature that must be withstood.

3) We have no way of telling where a bubble will occur, how far it will rise or when it will crash. Therefore, it is best simply to weather them.

4) It is easy to lament the cost of a bubble or the impact of buying expensive assets in hindsight; it is much more difficult to accept the years of painful underperformance which will come when we reduce our exposure early, yet the momentum continues. The behavioural challenges of an active approach are far too great to bear.

5) Country allocations based on market cap are a reasonable proxy for future earnings on average, despite being wildly inaccurate at times.

None of these arguments suggest that buying extremely expensive assets is prudent, rather they accept the drawbacks of a passive country allocation, whilst believing it to be the best (or least worst) option.

As guilty as active investors are of dismissing the evidence around the efficacy of index funds however, passive investors are equally culpable in rarely acknowledging the shortcomings they suffer. Even committed passive exponents should ask themselves whether there are any scenarios where index exposures become so extreme that they would be willing to go against everything they believe and take active positions away from the benchmark.

What would they do in a repeat of the Japan scenario?

Situations like the one we observed in late 80’s Japan will likely occur again; perhaps we are entering such a phase with the US.

It is easy to be complacent about the rise of US equities to close to 70% of the MSCI World Index. The strong performance that has led to it and the narratives used to rationalise it make extrapolation and justification easy. But we should not ignore that passive investors are becoming progressively more exposed to one of the most richly priced global equity markets.

So, is the US a Japan redux? No. The valuations are nowhere near as extreme (which is not really saying much) and the corporate fundamentals do justify a high US weighting. The FTSE RAFI Developed 1000 index, which weights companies based on factors such as dividends, cash flow and sales has a US equity allocation of c.59%. Not quite 70%, but even if we disregard stretched valuations, the US is still the world’s dominant equity market.

Not being Japan does not mean investors should blindly accept the situation. History would suggest that stretched valuations lead to disappointing returns. It is hard to argue that valuations in the US are not elevated (even relative to other regions).

I have heard passive advocates justify the increasing US weighting by making claims about US exceptionalism and the incredible profitability / market dominance of the tech and consumer names. Whilst this might be a credible case it is conflating an active investment view with the use of index funds. The correct argument – as mentioned above – is that this type of situation is a known and expected feature of a market cap, global equity allocation; and they believe it to be the best method for capturing long-run global equity returns.

—

There are many awful ways to invest that we should avoid at all costs, but there is also no right way -just a range of reasonable techniques all of which come with advantages and serious drawbacks. Most investors align themselves with a particular religion (active or passive) and summarily dismiss the other. This is unhelpful and belies the realities of hugely uncertain financial markets with often conflicting evidence.

In simple terms, passive country allocators need to accept that they will buy increasing amounts of punitively expensive assets; whereas active investors (at least those with a valuation discipline) will endure multiple years (maybe decades) of severe underperformance even if they are right in the end.

No approach is perfect, we must pick our poison.

Pingback: a range of reasonable techniques - Cazy Boy Tech

Pingback: Wednesday links: a range of reasonable techniques - AlltopCash.com

Pingback: Weekend reading: The office - Belman Partners

Pingback: Weekend Reading: The Office - Monevator - News07trends UK

Pingback: Weekend reading: The office - Monevator

Pingback: Weekend reading: The office - Comas Family

Pingback: Weekend reading: The office - Wealthy $imple

Pingback: Weekend reading: The office - Ubica Capital

Pingback: Weekend Studying: The Workplace - Monevator - Downmovie21

Pingback: Closet Indexers, Semantic Knots, and Quality Rules – The Investment Ecosystem

Pingback: Has the Rise of Passive Funds Really Broken Markets? | Behavioural Investment