It is easy to think about investment behaviour as a problem for the individual, a risk that we need to manage to avoid poor choices and costly mistakes. But it is much more than that. The challenges that we encounter as solo investors – our tendency to extrapolate, our susceptibility to stories, our obsession with random short-run outcomes (I could go on) – also operate in aggregate. They impact everyone. Major market anomalies arise because of group behaviour. If we want to exploit behavioural opportunities and avoid the risks, we need a framework for recognising them.

Identifying behavioural opportunities and risks is about comparing two critical facets of investment – evidence and expectations. Behavioural irregularities become apparent when there is a disconnect between what the weight of evidence tells us about a likely investment outcome and what market expectations are. What is in the evidence versus what is in the price. The greater the divergence, the greater the prospect or danger.

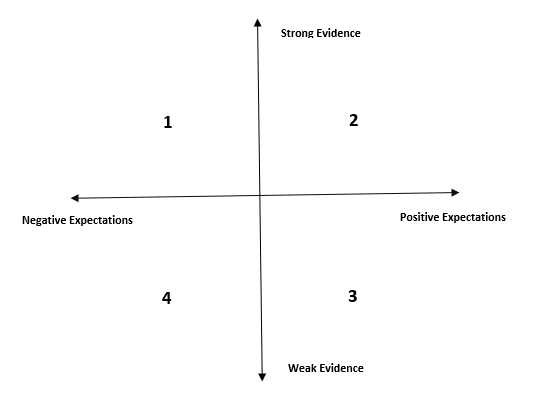

I will discuss in more detail how we should think about evidence and expectations later in the piece, but first I want to present a simple matrix that we can use for categorising where our investments sit from a behavioural opportunities and risks perspective:

Behavioural Opportunities and Risks Matrix:

The matrix is easy to use. For any investment we start by proposing a hypothesis, such as:

This asset class / fund / strategy will deliver above average returns over the next ten years.

We can then assess how strong the evidence is that this proposition is true, and whether market expectations for the investment are positive or negative.

Let’s take each quadrant in turn:

Quadrant 1: Strong Evidence / Negative Expectations: This is the most attractive area from a behavioural opportunity perspective, it is where robust evidence is seemingly in conflict with market expectations.

An example of this would be the value factor in equities in recent years. The evidence that there is a long-term premium attached to this factor is strong, but market expectations were dire – this could be seen in pricing, performance and general sentiment.

Such situations give investors two chances to benefit – the evidence that there is an additional return available in a steady state, plus the potential reversion of extreme market / behavioural positioning.

There is a problem, however. Although this quadrant presents the greatest opportunities, they are also the most behaviourally challenging. Market expectations conflict with the evidence – so if we follow the evidence most people will think we are wrong. The more extreme the market positioning, the greater the potential return, but the more intense the pressure will be to fold.

We can think of the returns in this area as – at least in part – a reward for the behavioural fortitude required for this type of informed contrarianism.

Quadrant 2: Strong Evidence / Positive Expectations: Here market opinion aligns with the evidence. There are solid reasons to believe an asset, fund or security should deliver favourable outcomes and market sentiment is consistent with that. Positive evidence allied to positive sentiment.

The major pitfall for investors with assets in this quadrant is where positive expectations become so fervent and valuations so stretched that this significantly dampens the prospective return – despite robust evidence of an investment’s efficacy. For example, our hypothesis might be that on a long-term (10 year+) view a market cap based global equity allocation approach is optimal, yet in situations such as the Japanese equity bubble when a market trading at near 100x cycle adjusted earnings made up close to 50% of global indices, that assumed advantage diminishes. Expectations can run so far that they can compromise an investment even when supported by reliable evidence.

Quadrant 3: Weak Evidence / Positive Expectations: This is the worst quadrant for (most) investors to be involved with. These are situations where the evidence supporting good outcomes is weak but the market is behaving as if the opportunity is incredibly attractive. In this type of scenario there is typically severe friction between evidence and stories. There is likely to be talk of ‘new paradigms’ for investments in this quadrant.

A prime example of this would be a star fund manager at an extreme positive in their performance cycle. The evidence would strongly suggest that funds that have generated extraordinary returns and hold stocks at astronomical valuations will go on to (severely) disappoint. Yet market expectations are telling us something different – inflows will be increasing, the manager will become prominent across all media outlets and narratives will be weaved about their otherworldly abilities. This scenario is a major behavioural risk for investors where the potential for catastrophic losses is very high.

Unlike quadrant 1, however, this type of investment will be behaviourally comfortable, perhaps even exciting. The broad evidence about funds with stellar performance will be roundly ignored, in favour of the far more exciting stories that will be told about this specific manager. And, of course, it will be persuasive because the track record is so strong!

Quadrant 3 should only be a hunting ground for momentum investors, who are interested in the price trend of an investment rather than the fundamental evidence. The behavioural fervour should present an investment opportunity, and they should have the rules and disciplines to exploit it dispassionately. Everyone else should avoid.

Quadrant 4: Weak Evidence / Negative Expectations: This quadrant is where investment stories go to die, and is a short seller’s paradise. Not only is there weak evidence supporting an investment delivering good outcomes, but market expectations have soured and now support that view.

A recent example of an investment residing in this quadrant is ultra-high growth companies over the past eighteen months, which have moved from quadrant 3 to quadrant 4. There is scant evidence that expensive, growth companies deliver good long-run outcomes and market sentiment has turned dramatically against them. This is a toxic combination.

Quadrant 4 is where a behavioural risk has been realised.

There are potentially opportunities here for short sellers, and also for naive contrarians who will invest on the basis that expectations have become simply too negative.

Moving Between Quadrants

As is hopefully apparent, profits and losses from behavioural opportunities and risks are generated primarily when an investment moves across quadrants because of changing expectations. Profits will be realised from a movement between quadrants 1 and 2, whereas losses will be incurred in the shift between 3 and 4. The gap between expectations and evidence closes, either positively or negatively.

What is Evidence?

While the matrix is designed to be simple, the decisions about where an investment should sit will often not be (although at times it might seem obvious). The first challenge is judging the strength of evidence. This is not about deciding on its validity alone, but which evidence to use.

The best way to think about this problem is to delineate between two types of evidence – an outside view and an inside view. The outside view will be the general evidence from history about similar situations. In the star fund manager example I used to explain quadrant 3, this would be looking at all previous instances where funds have delivered comparable levels of excess returns or had similar valuations. This would form our base rate – on average what does future performance look like for funds with these characteristics?

We can complement this with an inside view. These are the details specific to this particular investment. The features of the fund manager, environment and portfolio that might provide relevant insights.

Our tendency is to heavily overweight the inside view because it is more salient, recent and compelling, but this is entirely the wrong approach. The assessment of the strength of evidence should be heavily biased towards the outside view, with a modest adjustment from the inside view. We should not make an investment without taking an outside view and understanding the base rates involved.

What are Expectations?

Although the idea of market expectations seems quite nebulous and difficult to define, in some ways these are easier to judge than the evidence. I would simply look at three factors to quantity expectations: performance, valuation and momentum. If medium-term returns have been abnormally robust, valuations are rich relative to history and shorter-term momentum (under 12 months) strong then it is easy to tell where expectations are, with the reverse also being true. The more extreme these measures, the more likely there are to be behavioural opportunities and risks present.

Extremes Matter

Extremes are incredibly important. Most of what we see in markets is noise – normal, random variation around some long-term trend or average. It is impossible to make judgements about such fluctuations and they should be largely ignored. It is when expectations and opinion reach extreme levels that behavioural risks and opportunities will become acute. This is because taking contrary positions against unjustifiable extremes is so difficult – running counter to the crowd is against our instinct and most likely our incentives. Going against the evidence and following outlandish expectations will feel comfortable but come with a heavy behavioural tax.

It is impossible to define what an extreme is (although we will probably know it when we see it). We might want to define specific levels or merely just monitor valuation, performance and momentum relative to an investment’s history – there is no perfect way to approach it. Whatever strategy we adopt for identifying extreme expectations, we will never accurately call the peak or trough.

Not a Timing Tool

Though it is possible to observe extreme dislocations between expectations and what the evidence tells us, we will not be able to successfully judge when such a gap will close (unless we are incredibly lucky). Extremes can persist for longer than we think and become more extreme than we ever felt reasonably possible. This presents a particular problem because sensible, evidence-based decisions can look quite the opposite for prolonged periods of time.

There are two important consequences that stem from our inability to time markets, even when the evidence strongly supports out view: i) We must be aware of our behavioural tolerance for investment views to continue to move against us, even when things appear detached from reality. ii) As investors we should not be trying to make heroic calls on markets, but merely make sensible decisions that will work on average through time, while avoiding disasters. We are trying to get the odds on our side, rather than bet everything on 15 black.

What Does it Miss?

The main limitation of this approach to identifying behavioural opportunities and risks is the potential to misjudge the evidence. We might use the wrong evidence – such as an incorrect, biased sample – or overweight specific parts, such as the inside view. The evidence we use should be as impartial as possible, but of course the way we search for it and decipher it will be influenced by our own priors and preferences.

The other issue is where there is a gap between evidence and expectations, but it closes in the opposite manner to what we expect – the evidence comes to meet with expectations. This will be a ‘paradigm’ or ‘regime’ shift situation, where historic evidence is no longer (or at least less) relevant. Of course, whenever market expectations are stretched and diverge materially from the evidence it always feels like a paradigm shift, until it doesn’t. We can be successful investors without ever predicting such unlikely events.

Who Can Use It?

This approach to identifying behavioural opportunities and risks might seem quite niche, but it is relevant to all investors. Understanding evidence and market expectations is central to any decision that we might make. Even investors who want to reside firmly in quadrant 2 and have no appetite for the potential pain and anxiety that comes with the opportunities in quadrant 1 should still think in these terms – why? Because even the most strongly evidenced investment will at some point in time be out of favour and found in quadrant 1, or be enjoying such positive expectations its future returns are materially compromised. Also, at some juncture, we will inevitably be lured towards the spectacular stories being told about the investments that sit in quadrant 3. Thinking about where our investments are in the matrix can help us manage the challenges of such situations.

Understanding Behavioural Opportunities and Risks

While understanding and controlling our own behaviour is paramount to good, long-term investment outcomes; we cannot ignore the behaviour of our fellow investors. Indeed, our own actions are typically a response to the aggregate behaviour of other market participants – the choices made, and the stories told. Not only do we tend to focus overwhelmingly on the expectations and behaviours of others at the expense of the evidence, but we make the wrong inferences about those expectations – assuming that extreme positive returns in the past are a prelude to similar results in the future, being the prime example.

If we want to make the most of the opportunities that arise from investor behaviour and avoid the risks, we need to assess the evidence supporting our investment decisions and judge how they compare with investor expectations.

Watch for the gaps.

—

I have a book coming out! The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can find out more here.

Pingback: This Week’s Best Value Investing News, Podcasts, Interviews (7/22/2022) | The Acquirer's Multiple®

Pingback: BuzEditoriale 22 luglio 2022 - Elon Musk abbandona i Bitcoin. È tempo di abbandonare la nave? - BuzWay.it

Pingback: This Week’s Best Value Investing News, Podcasts, Interviews (7/22/2022) – Money Street News

Pingback: How To Identify Behavioural Investment Opportunities and Risks - Trading Game