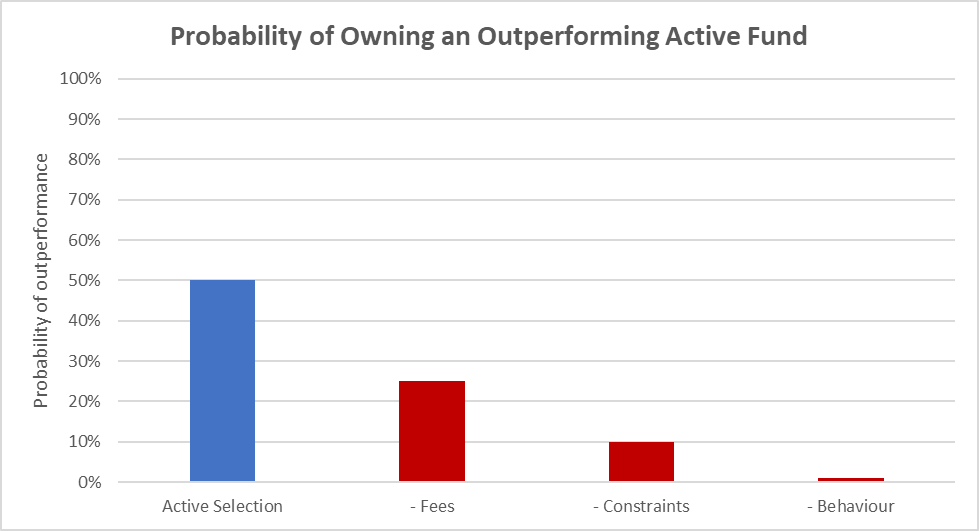

Selecting an active fund that will outperform its market capitalisation benchmark through time is an exacting challenge. We have all seen the bleak data regarding just how few funds deliver long-term excess returns in most (but not all) asset classes. It is, therefore, easy to make the argument that markets are simply too efficient and there are not sufficient opportunities for active investors to exploit, but this doesn’t hold water. Even if markets were efficient, we would expect a reasonably even distribution of outperformance and underperformance from active investors around this. Results would be random, but the probability of success would be somewhere near 50%. * In most cases, however, the odds of a positive outcome are far worse than this. But why?

There are three major issues that shift the probability of successful active fund selection from a 50 / 50 shot to something that can be close to zero: Fees, constraints, and behaviour. Any investor in active funds must manage these deliberately and well to give themselves a fighting chance:

Fees

Fees are the immutable, overwhelming impediment to successful active fund investing. They are a minor problem over any given year, but compound into a major, often insurmountable hurdle through time. The higher the fee level, the closer the probability of outperformance gets to zero.

People often misattribute the struggles of active management with efficient markets or incompetent professional investors, but this is generally not the case. The trouble is fees. Active funds are too expensive in aggregate, and this shifts our starting odds of success far lower than the 50% they would be before costs are considered.

In recent times there has been a conflation of two arguments: that low fees are incredibly beneficial to investors and that a market cap allocation approach is inherently superior to other methodologies. The first contention is true, the second is not. This mistaken thinking has arisen because most low-cost funds adopt a market cap indexing approach, and this methodology has enjoyed a prolonged period in the sun in many markets (the US in particular). There have been decades in the past where a market cap allocation has been inferior to other techniques (such as equal or fundamentally weighted).

The point is not that a market cap allocation is a poor strategy to adopt (it is perfectly sensible for most investors) but rather that the travails of active funds are more to do with the structural problem of high fees, rather than the cyclical issues of mega cap US companies making market cap indices hard to beat.

Staunch advocates of active fund investing often tend towards complacency on fees on the basis that certain managers are so skilful and will generate such a high level of alpha that the fee level isn’t a major concern. This is a dangerous mindset.

It is inconsistent to compare a certain cost with an uncertain benefit. If fees for an active fund are 1% and expected alpha is 2%, we need to haircut that forecasted outperformance for our own fallibility. We might be wrong that a manager has skill, or invest at an inopportune time (following a spell of stellar performance, for example). Active fund investors often talk about the hit rate required to be a successful fund manager (not much more than 50%), is it that different for fund investors? **

For active investors, reducing fees paid is the easiest lever to pull to improve the odds of success.

Constraints

Active fund investors must also seriously consider the constraints they encounter in their investment approach; these will substantially reduce their chances of delivering the desired outcomes.

The most obvious impediment is likely to be size. The larger the level of assets, the narrower the opportunity set and the more difficult it becomes to generate outperformance. Although (for obvious reasons) asset management companies do not like to acknowledge it, it is an inescapable fact that above a certain minimum viability threshold a rising level of assets impairs future returns. The extent of this hindrance will vary depending on the asset class involved but in almost all instances it is a major drawback.

It is not only size that serves to constrain active fund investors, but there is also a host of other implicit and explicit limitations that will impair returns and reduce the likelihood of success. ESG restrictions are an obvious area in the current climate, as are controls on variables such as tracking error or manager tenure. A requirement to recommend or own too many funds is also highly problematic (investment skill, if it exists, is scarce not abundant).

Some fund investors must even deal with disastrous constraints such as only holding funds that have delivered outperformance over certain historic periods (such as the last three years). This is the type of constraint that immediately puts the chances of long-run success at zero.

Anything that restricts the investable universe or limits the agency of the investor reduces the probability of successful active fund investing. It is critical that we know what these are before we start.

Behaviour

Even if we have skill in selecting active funds, manage fees prudently and face limited constraints, there is one thing that can make it all redundant – our behaviour. Active fund investors must be acutely aware of behavioural challenges (and be able to deal with them) if we are to have any hope of prolonged success.

The most significant behavioural challenge is related to time horizons. To invest in active funds there must be a willingness to not only hold for the long-term (we should be thinking ten years) but withstand the inescapable bouts of prolonged underperformance that will occur during these periods. Let’s be clear, on the time horizons and incentive structures of most fund investors, Warren Buffett would have been fired on numerous occasions.

An obsession with noise-laden short-term numbers – such as poring over quarterly results – or a bizarre fascination with the spurious idea of consistent calendar year outperformance are the type of traits that will eviscerate our chances of long-run success.

When owning an active fund for the long-term we will be regularly provided with reasons to sell. If an active fund manager has underperformed for three years, we will always be able to identify ‘process issues’ that have caused the underwhelming returns, and will not resist the urge of asking them “what are they doing?” to address their poor results (in most cases, hopefully nothing).

The added problem is that there will, of course, be times when selling is the correct course of action. Nobody said it was easy.

It is vital not to underestimate the harsh behavioural realities of active fund investing, but unless we are able to discard the rampant myopia and find ways to manage our preoccupation with short-run outcomes, we should be investing in index funds.

Improving the Odds of Success

This post has been somewhat negative as it has focused on those factors that make successful active fund investing so difficult, rather than address the positive steps that can be taken to improve the odds of success. Although I will cover this in another post in more detail, there are ways in which this can be done. Tilting towards empirically sound factors at a low cost (such as value, momentum and quality) should enhance long-term outcomes, identifying investors with skill is difficult but possible (it has little to do with past performance) and making counter-cyclical decisions (investing when valuations are cheap and performance is poor, rather than the reverse) is a painful but productive approach.

The problem is that the proactive measures we might take to improve our odds are irrelevant unless we first deal with high fees, burdensome constraints, and poor behaviour. These will conspire to overwhelm any other positive actions we might take. If we want to invest in active funds, we need to be clear about how we are going to address these three key issues. If we cannot then we really should not be doing it.

*This is a deliberate simplification, which assumes no skew (lots of small funds outperform and a few large funds underperform, for example) and that active investors invest only in their defined market.

** It is, of course, not just a hit rate that matters but the win/loss ratio too.

—

I have a book coming out! The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can find out more here.

Pingback: Tuesday links: the easiest lever to pull - AlltopCash.com

Pingback: Weekend Reading: How To Get Time On Your Side - Monevator - Daily News Era

Pingback: Weekend Reading: How To Get Time On Your Side - Monevator - UK Prime News

Pingback: Bacaan Akhir Pekan: Cara Menemukan Waktu Anda – IDN Rujukan News

Pingback: Weekend reading: how to get time on your side - Laolita Group

Pingback: Weekend reading: how to get time on your side - Belman Partners

Pingback: Weekend reading: how to get time on your side - Ubica Capital

Pingback: Weekend reading: how to get time on your side - Comas Family

Pingback: Weekend studying: how one can get time in your aspect - Yeah Daily

Pingback: Weekend reading: how to get time on your side | Big Money Investing

Pingback: Weekend reading: how to get time on your side - My Intermix

Pingback: The Infant Learner: 24 September 2022 – The Infant Learner