I am apprehensive about writing a post that is critical of performance benchmarks for active management as accountability is of paramount importance and comparing returns to a relevant benchmark is a valuable means of assessment. With those caveats in place, I now wish to argue that our use of benchmarks – specifically for short-term* performance measurement – is a major behavioural problem and one that transforms the job of active management from difficult to close to impossible.

The simple, but critical, point is that the way in which we measure something can have a profound impact on our behaviour, and be of detriment to our ultimate objective even if the measure is optically sensible. Many of us will have heard stories confirming this idea – in the United Kingdom the imposition of hospital waiting time targets by the National Health Service (NHS) has consistently backfired, with behaviours often directed toward hitting the specific target, at the expense of all else (a case of Goodhart’s law in action**). This issue is discussed in a paper by Bevan and Hood (2006), which compares the NHS situation to measures of productive output in the Soviet Union, which were also blighted by ill-judged performance targets and unintended behavioural consequences.

For active management the situation involves taking a reasonably effective (albeit imperfect) measure of success (long-term performance versus a benchmark) and then employing that same measure over a much shorter-time horizon, a period for which it is often devoid of meaning. The view seems to be that if it is a valid measure over the long-term then it can also be assessed over far more limited periods. If we can measure it over five years, why not three months, one month, one day? A significant amount of time is wasted and behavioural damage wrought by constantly appraising noisy short-term performance data.

If there is any skill in active management, then it can only be identified over the long-term; short-term performance numbers are a sea of randomness searching for a narrative. To validate this point, let’s take Michael Mauboussin’s simple heuristic for judging whether an activity is more driven by luck or skill – can you fail deliberately? For active investment management, over the short-term, the answer is absolutely not; it would be impossible to confidently select a portfolio of securities that would underperform over a day or even three months (it is entirely random), however, over the long-term it might just be possible. Certainly as the time horizon extends someone with skill in the field should have greater confidence in meeting this threshold.

Of course, the challenge for active management is that short-term performance data is available, so therefore we feel compelled to measure it, analyse it and assess it. I find it constantly baffling that anyone believes there is much information of substance such performance numbers, the only obvious exception being where relative performance diverges from what one might reasonably expect given the approach adopted by the fund manager. To believe that short-term returns tell you anything about the skill of an active manager, is to believe that certain individuals have the ability to predict short-term market movements. They don’t.

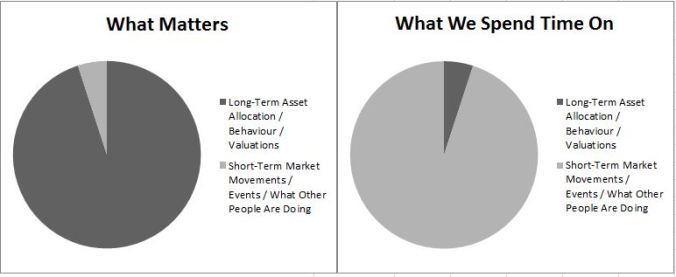

The problem with short-term performance analysis is not simply that it is a weak measure and rarely constitutes meaningful evidence, but that it has come to dominate investment thinking and decision making. Unfortunately, long-term outcomes are reached by experiencing and reacting to many periods of short-term performance.

How do active fund managers react to endemic short-termism? By reducing the risk they assume relative to their benchmark comparator. There is little point being a long-term investor, if you are fired after a year for ‘consistent underperformance’. There is great confusion at the heart of the debate around active management – on the one hand there is a drive for high active share managers who can justify their existence, but also a complete intolerance for spells of underperformance. These views are entirely incoherent.

Active management groups are interested in maintaining and growing assets. The dominance of closet trackers / index-hugging strategies is in part a consequence of the focus on short-term performance measures. Tracking errors are managed and ‘active risks’ are scrutinised as genuine active management is sacrificed and long-term decision making stymied to avoid descending to the foot of performance tables.

What are the consequences of professional fund investors’ use of short-term performance measurement? A great deal of entirely unnecessary activity. There is so much data available that it is irresistible; it is possible to construct all sorts of compelling narratives backed by supporting evidence and statistics. As fund investors we have every opportunity to scour daily / monthly / quarterly performance and make grand conclusions based on noisy and unreliable attribution. This brings us to a perennial problem of the investment industry – it is hard to prove your worth by doing less (even if it is the best course of action), being busy is often career-enhancing. It is easy to produce analysis that weighs a lot and means a little.

In defence of active fund investors, even if they wanted to focus on quality of process and genuinely long-term performance, they are often serving others for whom short-term performance is paramount. Why pick a high active share manager if you are likely to be hauled over the coals every other quarter to explain underperformance? Furthermore, remuneration will often be tied to the performance of funds recommended over time horizons where the outcomes can be considered no better than random. Most professional investors in active funds are incentivised (in the broadest sense of the word), to not take too much benchmark risk, be similar to everyone else and recommend funds with a strong recent track record that might still have some momentum.

Although I am often an advocate of doing nothing as a superior investment strategy, my criticism of the use of short-term performance measures is not about adopting a hands-off approach to active manager research, rather ensuring that the focus is on the right things. It is possible to have a granular understanding of an active manager without being consistently diverted by short-term vacillations in relative performance. Process must always trump outcomes; time should be spent understanding fund manager behaviour and whether it is consistent with expectations, not whether they have beaten a benchmark over some arbitrary period.

The basic message here is this – if you are worried about short-term relative performance, avoid active managers, if not you will spend a great deal of time making consistently poor investment decisions. For those committed to active management, it is imperative to put steps in place that support and foster it. This will often involve taking decisions that seem entirely counter-intuitive given how the investment industry has evolved in recent years. If you are employing or analysing short-term performance measures, you are inevitably shaping behaviour and reducing the chances of long-term success.

—-

* It is difficult to precisely define what is meant by long and short term and it depends on what you are talking about. For active management I would argue anything under one year is short-term and anything over five years is long-term. The bit in the middle we can debate.

** In simple terms, Goodhart’s law states that when a measure becomes a target it ceases to be a useful measure.

Key Reading:

Bevan, G., & Hood, C. (2006). What’s measured is what matters: targets and gaming in the English public health care system. Public administration, 84(3), 517-538.