Overconfidence bears the traits of many behavioural issues within investment – it is widely known, poorly understood and assumed to affect other people. Most of us are probably overconfident that we don’t exhibit overconfidence. Although there are memorable examples of overconfidence in action – such as the majority of people in a room believing they are an above average driver – there seems limited acknowledgement of what forms overconfidence can take or how it can influence our decision making.

The investment industry should be a fruitful area for identifying and understanding overconfidence. For a start there is an inevitable selection bias, I think it is safe to assume that the majority of individuals working in front office asset management roles exhibit more confidence in their own abilities than the general population. Furthermore, many investors engage in activities that are ripe for displays of overconfidence – economic forecasting and market timing (to name just two) are key pillars of the industry, despite limited evidence of their efficacy.

In the investment world overconfidence is a sought after characteristic. In an environment defined by uncertainty, we crave certainty, conviction and confidence (however ill-placed this might be); whereas circumspection, probabilities and caveats are associated with having a lack of knowledge or expertise. Thus, even if being well-calibrated is likely to improve your judgement, it will not necessarily have a similarly positive effect on your career prospects.

Whilst overconfidence is frequently discussed, there remains vagueness around what is actually meant by it; research by Moore and Healy (2008) sought to clearly distinguish distinct types of overconfidence*, defining these as: overestimation, overplacement and overprecision.

Overestimation: This is an overly optimistic view of our abilities or performance level. For example, we are likely to exaggerate the success of our investment decisions. As Moore and Schatz (2017) highlight, there appears to be a pattern where individuals overestimate their abilities on difficult tasks and underestimate on easy tasks. Investment would certainly fall into the former category.

If investors are overconfident about their performance level, what would be the benefit of such self-deception? One reason might be to manage the potential cognitive dissonance of believing yourself to be an intelligent and skilful investor, whilst simultaneously adding little value in your investment decision making – embarking on a career where you are no better than average may not be particularly fulfilling. Of course, such overestimation by investors might not be self-deception at all, but rather an effort to present oneself to others (clients and colleagues) in the most favourable light.

Overplacement: This is the classic ‘better than average’ perspective. Despite a litany of evidence on this phenomenon, Moore & Schatz (2017) highlight some limitations with the research in this area – most pointedly the fact that a skewed distribution can result in the majority of individuals in a sample being above average. They also argue that, unlike overestimation, overplacement occurs more for easy tasks with underplacement more common for difficult tasks.

Given that the investment industry is highly competitive and involves lots of people undertaking ostensibly the same tasks, my sense is that over-placement must be pronounced. Indeed, it might be something of a pre-requisite – if you are below average at active management or as an economist then there is seemingly not a great deal of purpose in that particular role. That is unless you take the view that there is so much uncertainty and randomness in investment that you can be aware that you are below average whilst pursuing a successful and well-rewarded career.

It may simply be the case that overplacement is somewhat irrelevant for asset management. It is perhaps so difficult to disentangle luck from skill, that nobody knows what the distribution of skill is or where they (or anybody else) falls within it with any sense of certainty.

Overprecision: This is exaggerating our knowledge of the truth, and is typically tested through calibration studies. For example, answering a selection of questions (such as estimating the length of the Amazon River) whilst employing a 90% confidence interval. Success rates are typically far lower than the prescribed confidence level.

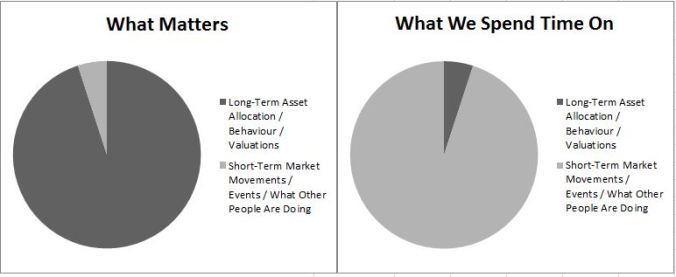

Overprecision would seem to be the most pervasive and pernicious form of overconfidence apparent in investment. Despite the inherently unpredictable nature of financial markets there is still an over-reliance on point forecasts, bold predictions and heroic portfolio positioning. The use of subjective probabilities around potential outcomes is also something of a rarity.

One way to address the issues of overconfidence is to talk more explicitly about confidence levels, probabilities and base rates when making decisions. Let’s take an example:

I decide to invest in an active equity manager and have based that choice on the manager’s strong historic track record, robust process and compelling investment philosophy – we can call this the inside view (evidence specific to this circumstance). Alongside this I must also strongly consider a base rate for active manager outperformance – in this instance over the last decade only 20% of the manager’s peer group have delivered performance in excess of the benchmark – we can think of this as the outside view (evidence incorporating a broader reference class).

To persist with recommending an active manager despite the base rate information means one of two things: i) I believe the base rate is anomalous and in the future the proportion of managers outperforming in this sector will increase, ii) I believe that my active management selection capabilities are sufficiently strong that I am willing to accept the highly unfavourable odds of identifying an outperforming manager (even before considering mean reversion in performance).

This is not to suggest that in these situations one should never go against the base rate, but rather it is critical to consider these factors when making such a decision. Failure to do so means we neglect crucial information, largely ignore probabilities and have no means of understanding the level of (over)confidence underpinning our decision making

For most investors it is sensible to make investment decisions on the assumption that our abilities are no better than average. We can do so by answering two questions:

1: Assuming I have no skill, what is the probability of a successful outcome?

To clarify the purpose of this question, I can make an adjustment to my earlier example – let’s assume that there was an asset class in which active management had historically been particularly successful and 70% of active managers had outperformed the index over the past decade. In such an instance, the odds of a positive outcome from selecting an active manager are in your favour (other things being equal) even in the absence of any particular skill in manager selection. This approach could apply to assumptions about future returns or, from a bottom-up perspective, company growth rates or margins. Whilst there might not be a perfect reference class or probability number for every investment decision, it remains a worthwhile exercise.

2: If I am taking a position where the odds are unfavourable, where do I hold a particular edge / skill and why?

When we take views that implicitly or explicitly reflect a high level of confidence in our own abilities, we should be clear about why this is the case. This is useful both for any given decision and also as a means of tracking decision rationale (and confidence) through time.

Overconfidence is a major issue for investors and can create a plethora of costly problems, such as insufficient portfolio diversification and overtrading. If, however, we think about our investment decisions on the basis that our skill is no better than average, we are far more likely to consider crucial factors such as base rates and put our own confidence levels into perspective. This is not a cure all solution for overconfidence, but should encourage us to make investment decisions when the odds are in our favour.

* I was reminded of this research by Jason Collins’ excellent blog.

Key reading:

Moore, D. A., & Healy, P. J. (2008). The trouble with overconfidence. Psychological review, 115(2), 502.

Moore, D. A., & Schatz, D. (2017). The three faces of overconfidence. Social and Personality Psychology Compass, 11(8), e12331.

Pulford, B. D., & Colman, A. M. (1996). Overconfidence, base rates and outcome positivity/negativity of predicted events. British Journal of Psychology, 87(3), 431-445.