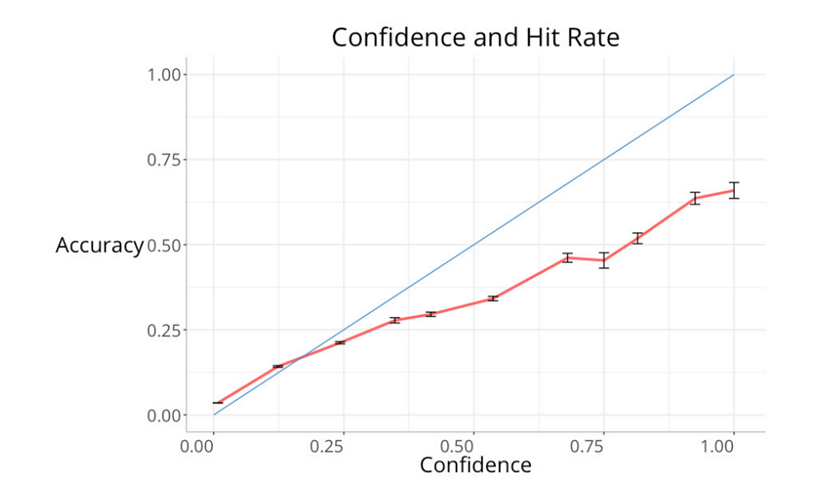

Although we might not like to admit it, we know that forecasting economic and market variables is tough, but just how tough? A new study by Don Moore and Sandy Campbell sought to answer this question.[i] They looked at 16,559 forecasts made in the Survey of Professional Forecasters since 1968, and found that those making expert predictions had 53% confidence in their accuracy but were only correct 23% of the time.

The study highlights the two central problems inherent in economic and market forecasting. It is not just that it is fiendishly difficult to get right (as the 23% shows), but we don’t appreciate how hard it is and are therefore poorly calibrated (the gap between 53% and 23%). This leads overconfident investors to make decisions based on unrealistic levels of precision.

One stark example in the study is that when forecasters held 100% confidence in their forecast, they were right only two-thirds of the time. Imagine the damage wrought by investment decisions based on an absolute confidence in the future. I am not even 100% sure the sun will rise tomorrow:

While the forecasters analysed in this study seem poorly calibrated, it is important to remember that they are doing things in the right way. They have expertise in their field, are adopting a probabilistic approach and receiving regular feedback on their quarterly forecasts. This is the correct method in making market predictions, yet overconfidence remains a major problem. Most investors making regular forecasts don’t have these attributes – we can only guess at the gulf that exists between their accuracy and confidence.

It gets worse still for investors. The study focuses primarily on single macro-economic variables – GDP, inflation and unemployment, but most investors are attempting to guess second order effects. How will ‘the market’ respond to changes in these factors. This adds another layer of unfathomable complexity to something that was challenging to start with.

Although the idea that forecasting is tough and people tend to be overconfident is hardly surprising, the results from studies such as these jar sharply with the everyday experience of financial markets, which are incessant stream of predictions. Investors are compelled to have a view on everything and must have conviction in that perspective.

But if we know that forecasting is incredibly difficult why can’t we stop ourselves from doing it?

Aside from simply thinking that we are better than other people, the primary reason is that predicting the future gives us comfort amidst profound uncertainty. It provides us a false sense of security in an environment that is incredibly chaotic. It is also expected of us – if everyone is making forecasts about everything then we should be too. Smart people are confidently foretelling the future – why aren’t we?

How can investors cope in a world where forecasting is endemic and expected, but very likely to lead to poor decisions?

Forecast the right things: Investors cannot simply stop making predictions. We all do it. Even the most ardent passive investing advocate is making implicit predictions about economic growth (economies will grow) and equity markets (equities will generate higher real returns than other asset classes) when building their portfolio. We should, however, be parsimonious in our predictions, modest in the assumptions required for our forecast to hold and have limited requirement for precision.

Focus on what matters: For most investors the list of things that actually matter to our long-run investment outcomes is far, far smaller than the things that we think will be of importance. To avoid getting caught up in the prediction machine, we should be clear about what these are from the outset.

Talk a lot, do a little: One of the reasons that forecasting is so prolific despite being so difficult is because investors always need something to talk about, and discussing financial markets can easily veer into forecasts about the future. It is okay to discuss about what’s happening in the world – in fact it might just be a requirement to keep people invested – but we should talk about markets far more than we do anything.

Understand we will be wrong, frequently: In the study, individuals with expertise, receiving feedback and taking a probabilistic approach were correct 23% of the time. We will be wrong far more than we think.

Prepare for a wider range of outcomes: It is not just that we will be incorrect, but the range of possible outcomes is likely to be wider than we will consider reasonable.

Be resilient to reality: We will be wrong more than we think and things will happen that are outside of our expectations, often by some margin. Our portfolio decisions and behaviour should reflect this.

Stop having views on everything: One of the most pernicious features of the investment industry is that everyone has to have a view on everything all of the time. Nobody can say – “I don’t know.” Given that forecasting is hard even for the best-prepared experts this is terribly damaging. We shouldn’t be asking why someone doesn’t have a view, but instead why they do.

Spend less time worrying about other people’s forecasts: Financial markets are populated by intelligent people making incredibly persuasive predictions. We should learn to ignore them. Rather than being captivated by a compelling view on the price of oil or the US dollar, we should instead be questioning why their ability to forecast is an exception to what the evidence so often tells us.

—

Nobody in financial markets will care that there is another piece of research highlighting quite how problematic forecasting can be, everything will continue as before. Investors who can, however, understand how hard it is and act accordingly will almost certainly be better off in the long-run.

[i] Overprecision in the Survey of Professional Forecasters | Collabra: Psychology | University of California Press (ucpress.edu)

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Pingback: Tuesday links: talking about markets - AlltopCash.com

Pingback: Tuesday links: talking about markets - QuantInfo - Empowering Algorithmic Trading Insights

Pingback: This Week’s Best Value Investing News, Podcasts, Interviews (03/22/2024) | The Acquirer's Multiple®

Pingback: Bacaan akhir pekan: Bung, di manakah harga rumah saya jatuh? – IDN

Pingback: The Infant Learner: 23 March 2024 – The Infant Learner