The dominance of US equities has been one of the most significant features of financial markets over the last decade. The sheer magnitude of outperformance makes it easy to claim that it has simply been a case of an in-vogue market enjoying a substantial and unsustainable valuation re-rating, but that’s not quite true. Although a material multiple expansion has been influential, fundamental factors – better growth and improving margins – have also been significant. There is a problem, however, with using these earnings advantages to justify the compelling relative returns produced by US equities. Implicit in these arguments is often the idea that it was obvious that this would happen, and now it is equally obvious that it will continue. This is where investors will likely come unstuck.

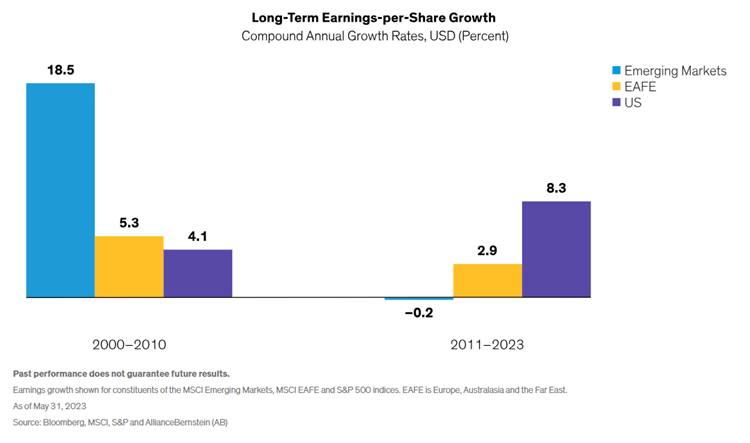

To explain why, we can look at this chart from Alliance Bernstein showing earnings growth across US, EAFE and Emerging Market equities:

How many people in 2010 were thinking – “over the next decade I believe US equities will be the place to be because of their earnings growth potential?” Not many. With the benefit of hindsight, we might think we were, but we weren’t.

Instead, we were likely to be saying: “Emerging market equity outperformance over the past decade wasn’t a bubble or about a valuation re-rating, it was about the fundamentals – haven’t you seen the earnings?”

In 2010, it would have felt obvious why emerging market equities had outperformed (‘it’s the fundamentals, stupid’) and that this would continue. It didn’t quite turn out that way.

These are the same arguments that are made now for US equities, but just applied to a different case at a different time. Our behaviours don’t change, just the subject that they are focused on.

There are two powerful and pervasive behavioural foibles at play here. Hindsight bias makes us feel as if the path we have taken was inevitable, whilst extrapolation leads us to assume that what has come before will continue. There is, however, something else that is just as problematic for investors – an inability to separate what matters from what is predictable.

Just because something will have a significant influence on the performance of an asset class, it does not follow that we can predict it with any level of confidence. Take earnings growth – this is a critical component of equity returns (the longer the horizon the more it matters) but is also incredibly hard to forecast. Just because something matters does not mean that it is a good idea to confidently forecast it.

Imagine attempting to estimate the relative earnings growth trajectories of emerging markets and the US back in 2010. That would require a wonderful ability to foresee developments in the growth of China, commodity prices and the rise of oligopolistic big tech firms (amongst a multitude of other things).

Added into this mix would have been the profound impact the strength of the US dollar has had on these fundamental fortunes. As currency forecasting ranks just below astrology in its accuracy, this makes life even harder. Earnings growth is really important, and it is also really important to understand our limitations in anticipating it.

When considering factors such as longer run earnings growth it is vital to accept that we are predisposed to be overconfident in our ability to forecast it and will also consistently assume that cyclical phenomena are structural. We should always start from a point of conservative assumptions based on long-run base rates and apply wide confidence intervals.

We must also remember that it should not be considered unusual for an outperfoming asset class to have had superior fundamentals. This is the critical part of the virtuous circle – better fundamentals – higher multiples – more persuasive stories. They feed on each other. The right question is not usually whether there has been any fundamental justification but whether it is sustainable and what is already in the price.

None of this is to say that the earnings advantage of the US will not persist. It is possible to make a perfectly plausible argument – probably around the rise of AI and the lack of effective antitrust enforcement – as to why this might be the case. It is, however, equally easy to contend that earnings are inherently cyclical and unusually strong tailwinds for certain markets (and industries within it) don’t tend to persist (they are unusual for a reason). This is without even considering starting valuations.

It is true that the outperformance of US equities over the past decade was heavily influenced by fundamental factors; it is not true that this was obvious before the fact, nor that it will necessarily persist. Anyone arguing otherwise is either wildly overconfident about their ability to see the future or trying to sell us something.

Things are never as obvious as they feel.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Pingback: Everything is Obvious - Trading Game

Pingback: Linkfest: 02 April, 2024 – Zack

Pingback: Irregular Roundup, 2nd April 2024 - 7 Circles

Pingback: This Week’s Best Value Investing News, Podcasts, Interviews (04/05/2024) – Daily Stock News

Pingback: Bacaan Akhir Pekan: Anda bilang Anda menginginkan kebebasan Anda – IDN

Pingback: Weekly Reading List - 11th of April - TAMIM Asset Management Concepts

Pingback: Weekly Reading List - 11th of April - TAMIM Asset Management Concepts

Pingback: The Infant Learner: 06 April 2024 – The Infant Learner