A topic I have changed my mind on during my career is concentration in funds. I used to be strongly of the view that it was only worth taking active investment positions if they came with high conviction – usually in the form of concentrated positioning – otherwise, what’s the point? Although I came to realise I was wrong about this, I am aware that many people far smarter than me remain advocates of this type of approach. Why do I think it is a problem when they don’t?

Fund concentration is not the easiest concept to define. There are obvious examples such as very focused equity portfolios with large weightings in individual companies, but there is more to it than that. Concentration doesn’t have to be about position sizes in stocks, it can come through an extreme sensitivity to a certain theme, concept or risk factor. It is about our exposure to specific and singular points of failure. Could one thing go wrong and lead to disaster?

The key concept to consider when thinking about the risk of concentrated funds is ergodicity. This is a horribly impenetrable term, but at its core is the idea that there can be a difference between the average result produced by a group of people carrying out an activity, and the average result of an individual doing the same thing through time.

Let’s use some simple examples.

Rolling a dice 20 times is an example of an ergodic system. It doesn’t matter if 20 people roll the dice once each, or an individual rolls the dice 20 times. The expected average result of both approaches is identical.

Conversely, home insurance is a non-ergodic system. At a group level the expected average value for buyers of home insurance is negative (insurance companies should make money from writing policies). So, why do we bother purchasing it? Because, if we do not, we expose ourselves to the potential for catastrophic losses. The experience of certain individuals through time will be dramatically different to the small loss expected at the average group level.

Investing is non-ergodic. Our focus should therefore be on our individual experience across time (not the average of a group); this means being aware of how wide the potential range of outcomes are and the risk of ruin.

In concentrated funds, the prospect of suffering irrecoverable losses at some point in the future is too often unnecessarily high.

‘Risk is not knowing what you are invested in’

One of the most common arguments made by advocates of running very concentrated equity portfolios is that it is an inherently lower risk pursuit because we can know far more about a narrow list of companies than a long list. If we have a 10 stock portfolio we can grasp the companies in a level of detail that is just not possible if we hold 100 stocks, and this depth of understanding means that our risk is reduced. The first part of this is right, the second part is wrong.

The problem, I think, stems from the fact that there are two types of uncertainty – epistemic and aleatoric. Epistemic uncertainty is the type that can be reduced by the acquisition of more data and knowledge. Here the idea of portfolio concentration lowering risk makes sense. Conversely, aleatoric uncertainty is inherent in the system; it is the randomness and unpredictability that cannot be reduced. It doesn’t matter how well we know a company or an investment, we are inescapably exposed to this. The more concentrated we are, the more vulnerable we are to unforeseeable events.

While I think a neglect of aleatoric uncertainty is at the heart of unnecessarily concentrated portfolios, there are other issues at play. Overconfidence is likely to be a key feature. we may be aware that the range of outcomes from a concentrated approach is wide, but that may be desirous to us because we believe that our skill skews the results towards the positive side of the ledger. Given our ability to fool ourselves and the aforementioned chaotic nature of the system, this seems to be a dangerous assumption to make.

Unfortunately, there is also an incentive alignment problem. A wide range of potential outcomes from an investment strategy becomes very appealing if we benefit from the upside but someone else bears the downside. This asymmetry is inevitably one of the reasons why high-profile macro hedge funds so often seem to be swinging for the fence with concentrated views. The often-severe downside of the negative outcomes are borne primarily by the client (a situation no doubt exacerbated when a hedge fund manager is already exceptionally wealthy).

Running a very concentrated investment strategy places an incredibly heavy onus on being right and also leaves us acutely vulnerable to unforeseen events unfolding that can have profoundly negative consequences. Exposing ourselves to such risks wilfully seems imprudent and unnecessary.

Investors are likely to overestimate how much they know, and underestimate how much they cannot know.

—

– Being wary of concentration does not mean increasing levels of diversification are always beneficial. There is a balance to strike.

– It feels important to note that the risk of concentrated strategies can be diversified by combining them, but we should still consider what the concentration levels say about the investor who is willing to adopt such an approach.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

A Tool for Testing Investor Confidence

Given how volatile and unpredictable financial markets are, thinking in probabilistic terms is an essential skill. It allows us to acknowledge uncertainty, express our level of confidence clearly and gives us more freedom to change our mind. There is a problem, however. Expressing ourselves in probabilities doesn’t come naturally and is often actively disliked. At best it is regarded as spurious accuracy, at worst evidence of an absence of conviction. We value bold and singular predictions about the future, not caveats and caution. How do we encourage probabilistic thinking in a world that doesn’t want us to?

One idea I happened upon in Julia Galef’s excellent book “The Scout Mindset”, is the ‘equivalent bet test’, which is a decision-making tool described by Douglas Hubbard in “How to Measure Anything”.

The concept is simple.

Let’s take a fairly generic claim that a professional investor might make. They think that the US ten-year treasury yield will rise above 5% before the end of the year. That’s great, but what does it actually mean? Are they certain that this will happen? (Given the historical accuracy of bond yield predictions, I hope not) Or are they only 51% sure? The difference matters a lot, but we have no idea. How do we find out? By creating an equivalent bet, where we are certain of the odds.

We say to our forecaster. There is now $100,000 at stake. We will give you this amount of money at the end of the year if your prediction on treasury yields is right. Alternatively, we will give you the same amount of money at the same time if you can pick a blue ball from a hat containing six blue balls and four red balls. You can only choose one of the bets – the treasury yield forecast or the drawing the balls from the hat.

If they decide to delve into the hat, then we know that their confidence in their bond yield forecast is less than 60%.

We can then adjust the ball selection bet to a point at which the forecaster is ambivalent about the two options. We then we have a reasonable guide to how confident they really are about their prognostications.

This is clearly an imperfect approach, a hypothetical $100,000 will almost certainly provide a different decision making response to a real sum of money, but it is likely to be broadly consistent and incredibly helpful.

Not only does the equivalent bet test encourage the forecaster to think about their judgment in probabilistic terms, it also provides a far greater level of clarity about both how confident an individual is and how well-calibrated (or not) they may be.

Whether we like it or not, we live in an uncertain, volatile and probabilistic world. Our decision-making approach should reflect this.

—

Galef, J. (2021). The scout mindset: Why some people see things clearly and others don’t. Penguin.

Hubbard, D. W. (2014). How to measure anything: Finding the value of intangibles in business. John Wiley & Sons.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

The Alpha Cycle

Industries in which capital has become abundant and optimism unbridled often end up disappointing investors. Echoes of these capital cycle pitfalls are also evident in active fund manager selection. In the ‘alpha cycle’ a certain area of the market delivers high returns, stories then emerge not only about the compelling opportunities to be found but also about the savvy investors who are exploiting them. This intoxicating mix of unusually strong performance and seemingly irrefutable narratives draws increasingly large flows from investors who either believe the tales being woven or are compelled to chase the momentum. The more extreme this performance dynamic, the more investors are likely to mistake luck for skill, and the cyclical for the structural. Leading them to make the wrong decisions at a terrible time.*

It is a curious phenomenon that investors seem to behave as if capital flooding into a certain type of fund (whether that be investment style or market subset) is a prelude to higher returns in the future. Of course, there is the potential to capture an ongoing trend, yet from a fundamental perspective abnormally high returns are likely to be the result of assets becoming significantly more expensive.

Exceptionally positive performance now is drawing returns from the future – we are not going to make them again. We just act as if we will.

At the heart of this alpha cycle problem is our propensity to believe that what is cyclical is in fact a structural shift. We are prone to see an active manager delivering strong performance in an in-vogue area of the market as someone with durable skill, rather than simply benefitting from largely unpredictable tailwinds that will at some point reverse. The most dangerous situation is when we begin to believe that there has been a permanent change in markets (XYZ is the only way to invest) and a particular active manager is the exemplification of this approach. Here we have the glorious opportunity to be wrong twice – about both markets and skill.

As flows into a certain style of active manager increase, so too does the clamour to invest and the belief that it is the obvious thing to do (performance doesn’t lie). As our prospective future returns dwindle, our conviction increases.

At points of performance extremes, whether an active manager has skill will become irrelevant. If they are investing in part of the market enjoying euphoric sentiment and following a period of unsustainably high returns, any edge will be overwhelmed by the almost inevitable reckoning.

Selecting active fund managers who have enjoyed prodigious tailwinds comes with twin challenges. First, we are likely to grossly overstate the presence of skill (we cannot help but conflate performance with skill). Second, even if they do possess an edge, it is unlikely to matter because the odds of investing successfully in an area that already has stretched valuations and delivered exceptional performance are poor.

We might argue that a fund manager has the ability to navigate such situations adroitly. Rotating out of areas that have delivered spectacular results and into less glamorous segments. Perhaps. Yet most managers have stylistic features or characteristics that almost inevitably leave them exposed to certain market trends. Furthermore, the type of fund managers that will attract the most attention during a particular cycle are likely to be the purest representation of whatever has been working.

The problems of the alpha cycle do present a potential opportunity. Fund managers with an out of favour approach who are investing in an unloved part of the market are likely suffering from poor performance and holding assets with far more attractive valuations. Even if they don’t have skill, the odds of a good outcome might be compelling (certainly better than investing at peak cycle).

There is a problem, however. We are very unlikely to believe managers somewhere near the trough of the alpha cycle have any skill, they are also likely to be haemorrhaging assets and they may be in danger of losing their job. It is never just a cycle remember; these are always profound structural changes at play.

I have framed the problems that stem from the cyclical nature of investment returns as an issue with active funds – it is not. These same behaviours exist across asset classes, regions and sectors. It is just that active funds have the additional danger of skill being used to justify unsustainable performance.

Investors need to adopt the mindset that unusually strong returns are a prelude to lower returns in the future and behave accordingly.

—

* I use ‘alpha’ in this article in the broadest possible sense – general outperformance, rather than anything more technical.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

The Curious Case of Catalysts

One of the most common questions I have heard through my investment career has undoubtedly been: “what’s the catalyst?” I have definitely asked it myself a few times but have tried to abstain in recent years. Most discussions around catalysts are an effort to anticipate what will change the view other investors hold about an asset – a pretty challenging task. We appear to believe that because catalysts seem obvious after the event, they must be predictable beforehand. This is a dangerous assumption.

There are two types of investment thesis – one about something that is already performing well, here a catalyst is unnecessary because we just need to extrapolate; the other is about something that isn’t working right now, and then a catalyst seems to become essential. The desire to identify a catalyst probably stems from our bias toward believing that current trends will persist, coupled with our discomfort at being uncertain – we want to know exactly how and when something will change.

It is worth taking a step back to consider what it is we are typically doing when identifying a catalyst.

There are three elements:

1) Predict an occurrence.

2) Predict how other investors will react to it.

3) Hold other things constant.

There are problems in each of these components – we are poor at making predictions about future events, we aren’t great at forecasting the reaction of other investors, and things are never constant. Other than that, we are all set.

Catalysts are asking us to specify in advance a specific driver of a change in the return profile of an asset or security. This is no easy task.

Although I am generally sceptical about catalyst predictions there are certain instances where it is more reasonable, particularly with micro-level decisions. For example, if an investor were to suggest that a company selling an underperforming unit could be a catalyst for higher returns to shareholders – this would seem specific and defensible (difficult but defensible).

The broader an investment view – I think US equities will start to underperform because X will happen – the more fanciful it seems. It just becomes far too complex. (I have looked back over my twenty-year career and found 476 catalysts identified for Japanese equity outperformance).

As with most things in investment decision making, the obsession with catalysts is, in part, a time horizon issue. If our horizon is appropriately long-term, we don’t need to predict what specific catalyst will change a certain investment’s fortunes, we can wait for the gravitational pull of fundamental factors to take hold (assuming we are right). The shorter our horizon the more sentiment matters – we are explicitly attempting to guess the behaviour of other investors, so we need a view on what might change that. (Short-term investing is hard).

It is safe to assume the success rate for identifying catalysts for potential shifts in the return profile of an investment is pretty low. We need to be right twice – about changing performance and the precise reason it will happen. The first one alone is hard enough.

If we are in the business of specifying catalysts, it would be prudent to keep a record of the judgements that we make through time. We may not like what we find.

At the start of this piece, I said that “catalysts seem obvious after the event”. The critical word here is “seem”. In most cases it is incredibly difficult to confidently specify the exact causes of a change in the performance of an asset even after it has occurred. We can certainly tell a great (and simple) story as to why something has happened, but the truth is almost always more intricate. If we cannot do it with the benefit of hindsight, trying to do it with foresight feels unwise.

Will there be a specific catalyst that alters the return profile of an asset? Maybe. Can we identify it in advance? Probably not. Do we need to? No.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

New Decision Nerds Podcast – Dealing with Underperformance

𝗛𝗼𝘄 𝗺𝘂𝗰𝗵 𝘁𝗶𝗺𝗲 𝗱𝗼 𝘆𝗼𝘂 𝗴𝗶𝘃𝗲 𝗮𝗻 𝘂𝗻𝗱𝗲𝗿𝗽𝗲𝗿𝗳𝗼𝗿𝗺𝗶𝗻𝗴 𝗶𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁 𝗺𝗮𝗻𝗮𝗴𝗲𝗿?

1. Hire a manager after a period of strong performance.

2. Watch in discomfort as you don’t experience that performance, maybe the opposite.

3. Spend a huge amount of thinking time and emotional labour working out why it wasn’t your fault.

4. Sack the manager.

5. Rinse and repeat with potentially similar outcomes.

Now that might not be you, but it is a story that plays out regularly.

Experiencing underperformance is one of the unavoidable realities of hiring an active manager. And it’s painful for everyone; clients, managers and advisers. And badly managed pain creates some predictably bad outcomes for all parties.

One important and manageable issue is time horizon mismatch. And this is what Paul Richards and I explore in the latest episode of Decision Nerds (link in comments). We explore:

𝗪𝗵𝘆 𝗶𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁 𝗲𝗱𝗴𝗲 𝗶𝘀 𝗻𝗼𝘁 𝗲𝗻𝗼𝘂𝗴𝗵 – managers need an appropriate amount of time to let their edge play out (if indeed they have one at all). It may be longer than you think.

𝗧𝗵𝗲 𝗕𝘂𝘅𝘁𝗼𝗻 𝗜𝗻𝗱𝗲𝘅 – a simple way of articulating time frames that can help everyone.

𝗘𝘃𝗲𝗿𝘆𝗼𝗻𝗲 𝗵𝗮𝘀 𝗮 𝗽𝗹𝗮𝗻 𝘂𝗻𝘁𝗶𝗹 𝘁𝗵𝗲𝘆 𝗮𝗿𝗲 𝗵𝗶𝘁 𝗶𝗻 𝘁𝗵𝗲 𝗳𝗮𝗰𝗲 – we posit that most people’s ability to predict how they will deal with the pressure of underperformance won’t reflect reality when things get tough.

We talk about the distinct behavioural pressures facing clients, advisers and managers and what they might consider doing to make things easier.

Available in all the usual places and below:

https://www.buzzsprout.com/2164153/14941612-underperformance-everyone-s-got-a-plan-until-they-re-hit-in-the-face

An Investor Checklist for Dealing with Geopolitical Risk

When investors consider the financial market impact of rising geopolitical risks the key underlying principle should be the late, great Daniel Kahneman’s maxim that: ‘nothing in life is as important as you think it is, while you are thinking about it’. That is not to suggest that such issues don’t matter, it is simply that they are likely to be less influential on our long run objectives than we think, and even if their impact was to be material our ability to navigate such situations well is highly questionable. Quite simply when we focus on issues that are high profile and salient, we tend to make poor decisions.*

When a geopolitical risk arises our natural tendency is to immediately become foreign policy experts, and also believe that we can confidently link complex and imponderable political situations to financial market outcomes. It is hard to overstate quite how difficult this is.

As is typical for investors, we treat each new event as an isolated incident and develop a convenient amnesia about similar situations in the past, which have either had limited long-term consequences, or where the impact was incredibly difficult to foresee.

It is not enough for something to matter, we must be able to predict it with some degree of confidence.

So, how should investors deal with geopolitical issues and the emergence of other high profile risks?

To keep something of a level-head amidst the noise and tumult, a checklist can be helpful. We should consider the following:

1) Do I have confidence in predicting the outcome of the current situation?

2) Do I believe I can predict the financial market implications?

3) Are any of these financial market implications likely to be material over my investing horizon?

4) Does my portfolio remain appropriately diversified for a range of different outcomes?

5) Has there been any change to my investing objectives?

In most situations and for most investors, the checklist should result in there being a limited response to emerging geopolitical risks and other types of potential market shocks.

This sounds easy, so why is such an approach difficult to apply?

There is, of course, the incessantly damaging perception that if something is on the front pages, investors should be ‘doing something about it’, but there is an even more pernicious problem. At some point a geopolitical risk will have a major financial market impact, and we cannot face the prospect of having done nothing about it.

The fear of doing nothing whilst something important is unfolding is a real one, and leads many investors (often professionals) to make incredibly poor choices. When considering this conundrum, we need to ask ourselves two questions:

1) Even if we assume that an event will have a meaningful impact on financial markets, how confident are we that we can manage it adroitly? It is a herculean assumption that we will make good choices through a period that is likely to be chaotic, stressful and unpredictable.

2) Will we know in advance which of the many such geopolitical events will be genuinely consequential? On the very solid assumption that we won’t, this will mean that we must constantly trade around such situations – just in case it is the one that matters.

Although it might be quite difficult to acknowledge, anyone who has lived through financial markets for any period of time will know that Kahneman’s maxim is right. We lurch from one potential major risk to the next, almost always overstating its importance and each time making some ill-judged predictions. Investors need to worry less about geopolitical events, and more about the poor decisions we will make because they are the focus of our attention.

—

* Hopefully, it goes without saying that when I am writing about how much such issues matter it is purely from a financial market perspective. The human costs and implications are often profound and far, far more important than any investing consequences that may transpire.

–

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Why is it so Easy to Disregard Behavioural Finance?

Behavioural finance has a problem. People talk about it a lot, but use it a little. If anything, improvements in technology and communication has made good investment behaviour even more challenging. Both the temptation and ability to make bad choices has never been greater. The central issue that behavioural finance faces is that – at its core – it is asking investors to stop doing things they inherently and instinctively want to do (and are in many cases are paid to do). That is an exceptionally hard sell.

If we take a deliberately simplistic approach to grouping some of our most problematic investing behaviours, we can see what makes adhering to the lessons of behavioural finance quite so tough:

We do things that are emotionally satisfying and anxiety reducing: Many of our actions – such as selling poorly performing funds or assets, or reacting to short-term market events – make us feel much better in the moment.

We do things that play to our ego: We want to believe that we are better than other people and this overconfidence leads us to engage in activities with horrible odds such as market timing,

We do things because of what other people are doing: We are social animals and take decisions because we want to be like other people or compare favourably to them.

We do things that are easy: We are cognitive misers and prefer simple explanations. That’s why we are so keen to translate a complex financial world into simple stories.

We do things that had evolutionary benefits: This one could really cover everything. Most of our worst investing behaviours are effective evolutionary adaptions and useful in many other contexts. Worrying about the short term and obsessing over recent events is great for our survival but not so good for meeting our long-term investing outcomes.

Viewed through this lens it is easy to see why encouraging people to think more about their behaviour is such a challenge. We are asking them to do the following:

- Stop doing things that give them immediate satisfaction and reduce stress.

- Accept that they are not as smart as they think they are.

- Stop looking at what other people are doing.

- Accept that markets are complex and unpredictable.

- Ignore most of what has your attention right now.

The idea that applying behavioural finance concepts is easy is nonsense. It is far far easier to give in to our ingrained dispositions which are natural and make us feel good – that’s why everyone does it. Improving our investing behaviour means going against our own instincts and often what other people are doing.

What makes matters worse is that the industry encourages and validates our natural and problematic behaviours. Lots of value accrues to turnover, stories, short termism and irrelevant comparisons. When I say value, I mean fees – not performance.

Another issue is that applying behavioural finance concepts has no immediate payoff, so it can be difficult to articulate its true worth. Any value that will accrue will take time and there is no obvious counterfactual. There is no benchmark for the poor decisions we would have made without it (a problem made harder by the fact they we will never accept that we would have made those poor decisions).

It is important to remember that behavioural finance would be redundant if it were easy; if it wasn’t hard it wouldn’t be useful.

Applying behavioural finance well is a skill. One that involves developing a plan that will ask us to act against what we think is our better judgement. We will struggle to evidence its value and there will be times when it looks like it doesn’t work at all – “why did you tell me to sit through a bear market when I could have got out at the top!?”

Absolutely integral to accruing the benefits of understanding and managing our behaviour is moving away from the idea that it is about simply doing nothing and ignoring markets. This might work for some but for most it is not realistic. Instead, it is about defining which types of behaviour add value and identifying those which are destructive ahead of time. This requires constant work and effort. It is not solely about creating disciplines but also continually reaffirming why they are in place. The concepts will be incessantly stress tested by fluctuating markets and ever-changing narratives.

Our default state is to disregard the lessons of behavioural finance. It is simply how we are wired. There are, however, huge benefits to be unlocked if we can take the time and effort required to engage with them. Our behaviour remains the most important factor influencing our long run investing outcomes, let’s not ignore it.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Active Investors Need to Think About the Odds

Although investing is far noisier and uncertain than most card games, it is also an activity where understanding the odds is critical. While investors may feel uncomfortable talking about their decision making in probabilistic terms, it is inherent in everything we do – whether we are explicit about it or not. Much like assessing our chances in a particular game of cards, active investors should be asking themselves three questions before making a decision:

1) What are the odds of the game?

2) Do I have skill?

3) What hand have I been dealt?

Let’s take each in turn:

What are the odds of the game?

This is simply judging the expected long run success rate of an activity – on the assumption that I am an average player. If my objective is to win at a game, I want to play the one where the odds are most in my favour.

For active investors this is about seeking to identify the structural inefficiencies in a market that might create advantages relative to an index tracking approach. Although these dynamics might change through time, they should move at a glacial pace.

To take a simple example of what this could mean – I might assume that the odds of success for an active equity fund manager are better investing in Chinese A shares than US large cap equities. This is because the former has more retail participation and may price new information less efficiently (amongst other things). This may not be true (there are certainly reasons why active investing could be harder in the Chinese domestic market), but such issues should be at the forefront of our thinking.

This is clearly not an easy judgement to make and there will be no precise answer, but it makes no sense to invest actively without first at least attempting to consider the odds of achieving a positive outcome.

Do I have skill?

The structural odds of a game are our starting point, but they will be impacted by the presence of skill. A poker player with evident skill should win more over time. The problem for investing is that skill is difficult to judge and far, far more people think they have it than actually do.

Skill can be quite an emotive term, so it is probably better to frame it as an edge. If I am going to engage in an investment activity with average or underwhelming odds, then I need to have an edge to justify participating.

Investors have terrible difficulty talking about skill and edge, but it is essential to do so. It might be analytical, informational, behavioural or something different entirely, but it must be something. If my choices are consistent with me believing I have an edge, I need to be clear about what I think it is.

What hand have I been dealt?

Sometimes the structural odds of a game, or the influence of my skill in playing it, can be dominated by whether I am dealt a great or terrible hand.

As an investor I can think of these as cyclical or transitory factors that influence my chances of outperformance. This is nothing to do with the perennial promises of it being a “stock pickers’ market” or other such empty prophecies, but rather factors like observable extremes in performance, valuation or market concentration that arise at different points through time and may have a material impact on my fortunes.

The best recent example of such a scenario would be in 2020 when a select group of high growth, actively managed equity funds had delivered staggering outperformance against the wider market. They had generated astronomical returns and held stocks that traded on eye watering valuations. Investing in such funds at this time (which investors unfortunately desperately wanted to do) is the same as being dealt a terrible hand in a game of cards. It overwhelms everything else – the overall odds of the game and our level of skill become irrelevant. The probability of achieving good outcomes from such starting points is inescapably low.

Of course, such a situation is even worse than being dealt a bad hand in a game of cards because investors – buying into the story and beguiled by past performance – will play it like it is a great hand.

The sad truth is investors are more likely to go ‘all in’ with an awful hand and fold a great one.

—-

Investors seem to dislike thinking in probabilities. In part this is because it can feel like we are applying spurious accuracy, but more because it can betray a profound uncertainty about the future, which jars with our general overconfidence. Despite this discomfort, we cannot escape the fact that we are playing a probabilistic game. We will never get to the right answer, but it would help our decision making greatly if we at least tried to carefully consider what our odds of success might be.

–

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Everything is Obvious

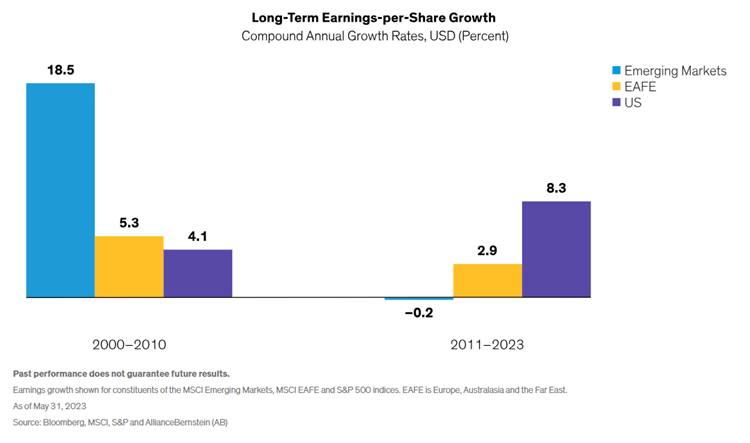

The dominance of US equities has been one of the most significant features of financial markets over the last decade. The sheer magnitude of outperformance makes it easy to claim that it has simply been a case of an in-vogue market enjoying a substantial and unsustainable valuation re-rating, but that’s not quite true. Although a material multiple expansion has been influential, fundamental factors – better growth and improving margins – have also been significant. There is a problem, however, with using these earnings advantages to justify the compelling relative returns produced by US equities. Implicit in these arguments is often the idea that it was obvious that this would happen, and now it is equally obvious that it will continue. This is where investors will likely come unstuck.

To explain why, we can look at this chart from Alliance Bernstein showing earnings growth across US, EAFE and Emerging Market equities:

How many people in 2010 were thinking – “over the next decade I believe US equities will be the place to be because of their earnings growth potential?” Not many. With the benefit of hindsight, we might think we were, but we weren’t.

Instead, we were likely to be saying: “Emerging market equity outperformance over the past decade wasn’t a bubble or about a valuation re-rating, it was about the fundamentals – haven’t you seen the earnings?”

In 2010, it would have felt obvious why emerging market equities had outperformed (‘it’s the fundamentals, stupid’) and that this would continue. It didn’t quite turn out that way.

These are the same arguments that are made now for US equities, but just applied to a different case at a different time. Our behaviours don’t change, just the subject that they are focused on.

There are two powerful and pervasive behavioural foibles at play here. Hindsight bias makes us feel as if the path we have taken was inevitable, whilst extrapolation leads us to assume that what has come before will continue. There is, however, something else that is just as problematic for investors – an inability to separate what matters from what is predictable.

Just because something will have a significant influence on the performance of an asset class, it does not follow that we can predict it with any level of confidence. Take earnings growth – this is a critical component of equity returns (the longer the horizon the more it matters) but is also incredibly hard to forecast. Just because something matters does not mean that it is a good idea to confidently forecast it.

Imagine attempting to estimate the relative earnings growth trajectories of emerging markets and the US back in 2010. That would require a wonderful ability to foresee developments in the growth of China, commodity prices and the rise of oligopolistic big tech firms (amongst a multitude of other things).

Added into this mix would have been the profound impact the strength of the US dollar has had on these fundamental fortunes. As currency forecasting ranks just below astrology in its accuracy, this makes life even harder. Earnings growth is really important, and it is also really important to understand our limitations in anticipating it.

When considering factors such as longer run earnings growth it is vital to accept that we are predisposed to be overconfident in our ability to forecast it and will also consistently assume that cyclical phenomena are structural. We should always start from a point of conservative assumptions based on long-run base rates and apply wide confidence intervals.

We must also remember that it should not be considered unusual for an outperfoming asset class to have had superior fundamentals. This is the critical part of the virtuous circle – better fundamentals – higher multiples – more persuasive stories. They feed on each other. The right question is not usually whether there has been any fundamental justification but whether it is sustainable and what is already in the price.

None of this is to say that the earnings advantage of the US will not persist. It is possible to make a perfectly plausible argument – probably around the rise of AI and the lack of effective antitrust enforcement – as to why this might be the case. It is, however, equally easy to contend that earnings are inherently cyclical and unusually strong tailwinds for certain markets (and industries within it) don’t tend to persist (they are unusual for a reason). This is without even considering starting valuations.

It is true that the outperformance of US equities over the past decade was heavily influenced by fundamental factors; it is not true that this was obvious before the fact, nor that it will necessarily persist. Anyone arguing otherwise is either wildly overconfident about their ability to see the future or trying to sell us something.

Things are never as obvious as they feel.

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).

Forecasting is Hard and We Are Not Very Good At It. What Should Investors Do?

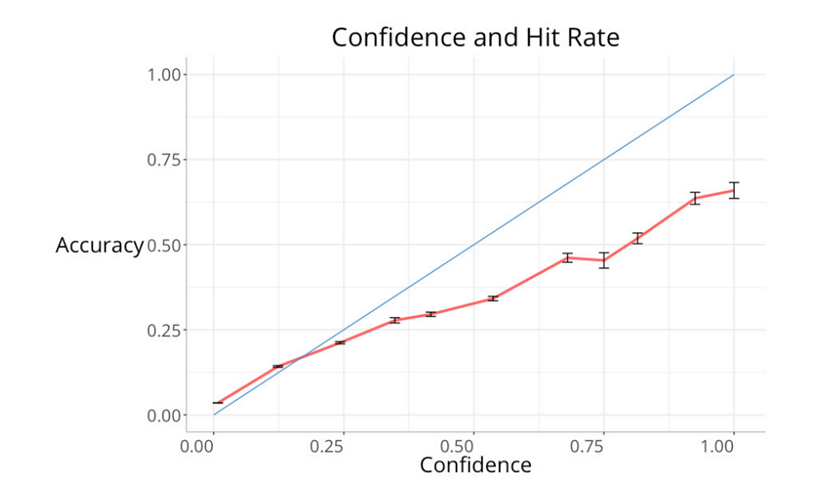

Although we might not like to admit it, we know that forecasting economic and market variables is tough, but just how tough? A new study by Don Moore and Sandy Campbell sought to answer this question.[i] They looked at 16,559 forecasts made in the Survey of Professional Forecasters since 1968, and found that those making expert predictions had 53% confidence in their accuracy but were only correct 23% of the time.

The study highlights the two central problems inherent in economic and market forecasting. It is not just that it is fiendishly difficult to get right (as the 23% shows), but we don’t appreciate how hard it is and are therefore poorly calibrated (the gap between 53% and 23%). This leads overconfident investors to make decisions based on unrealistic levels of precision.

One stark example in the study is that when forecasters held 100% confidence in their forecast, they were right only two-thirds of the time. Imagine the damage wrought by investment decisions based on an absolute confidence in the future. I am not even 100% sure the sun will rise tomorrow:

While the forecasters analysed in this study seem poorly calibrated, it is important to remember that they are doing things in the right way. They have expertise in their field, are adopting a probabilistic approach and receiving regular feedback on their quarterly forecasts. This is the correct method in making market predictions, yet overconfidence remains a major problem. Most investors making regular forecasts don’t have these attributes – we can only guess at the gulf that exists between their accuracy and confidence.

It gets worse still for investors. The study focuses primarily on single macro-economic variables – GDP, inflation and unemployment, but most investors are attempting to guess second order effects. How will ‘the market’ respond to changes in these factors. This adds another layer of unfathomable complexity to something that was challenging to start with.

Although the idea that forecasting is tough and people tend to be overconfident is hardly surprising, the results from studies such as these jar sharply with the everyday experience of financial markets, which are incessant stream of predictions. Investors are compelled to have a view on everything and must have conviction in that perspective.

But if we know that forecasting is incredibly difficult why can’t we stop ourselves from doing it?

Aside from simply thinking that we are better than other people, the primary reason is that predicting the future gives us comfort amidst profound uncertainty. It provides us a false sense of security in an environment that is incredibly chaotic. It is also expected of us – if everyone is making forecasts about everything then we should be too. Smart people are confidently foretelling the future – why aren’t we?

How can investors cope in a world where forecasting is endemic and expected, but very likely to lead to poor decisions?

Forecast the right things: Investors cannot simply stop making predictions. We all do it. Even the most ardent passive investing advocate is making implicit predictions about economic growth (economies will grow) and equity markets (equities will generate higher real returns than other asset classes) when building their portfolio. We should, however, be parsimonious in our predictions, modest in the assumptions required for our forecast to hold and have limited requirement for precision.

Focus on what matters: For most investors the list of things that actually matter to our long-run investment outcomes is far, far smaller than the things that we think will be of importance. To avoid getting caught up in the prediction machine, we should be clear about what these are from the outset.

Talk a lot, do a little: One of the reasons that forecasting is so prolific despite being so difficult is because investors always need something to talk about, and discussing financial markets can easily veer into forecasts about the future. It is okay to discuss about what’s happening in the world – in fact it might just be a requirement to keep people invested – but we should talk about markets far more than we do anything.

Understand we will be wrong, frequently: In the study, individuals with expertise, receiving feedback and taking a probabilistic approach were correct 23% of the time. We will be wrong far more than we think.

Prepare for a wider range of outcomes: It is not just that we will be incorrect, but the range of possible outcomes is likely to be wider than we will consider reasonable.

Be resilient to reality: We will be wrong more than we think and things will happen that are outside of our expectations, often by some margin. Our portfolio decisions and behaviour should reflect this.

Stop having views on everything: One of the most pernicious features of the investment industry is that everyone has to have a view on everything all of the time. Nobody can say – “I don’t know.” Given that forecasting is hard even for the best-prepared experts this is terribly damaging. We shouldn’t be asking why someone doesn’t have a view, but instead why they do.

Spend less time worrying about other people’s forecasts: Financial markets are populated by intelligent people making incredibly persuasive predictions. We should learn to ignore them. Rather than being captivated by a compelling view on the price of oil or the US dollar, we should instead be questioning why their ability to forecast is an exception to what the evidence so often tells us.

—

Nobody in financial markets will care that there is another piece of research highlighting quite how problematic forecasting can be, everything will continue as before. Investors who can, however, understand how hard it is and act accordingly will almost certainly be better off in the long-run.

[i] Overprecision in the Survey of Professional Forecasters | Collabra: Psychology | University of California Press (ucpress.edu)

—

My first book has been published. The Intelligent Fund Investor explores the beliefs and behaviours that lead investors astray, and shows how we can make better decisions. You can get a copy here (UK) or here (US).